Definition of Goodwill in Business: Value & Impact 2026

Get a clear definition of goodwill in business for owners. Explore personal vs. enterprise goodwill, valuation, sale price & tax impact.

July 8, 2026

July 15, 2026

Business synergy means the combined company creates more value than the two businesses could create on their own. In deal terms, that’s the “2+2=5” idea, and in M&A it’s measured as the present value of incremental after-tax cash flows from the combination, net of costs and risks.

If you’re an owner, you’ve probably heard the word in a buyer meeting and wondered whether it means real value or polished sales talk. That’s a fair reaction. “Synergy” gets used so often in deal conversations that it can sound like banker wallpaper. But underneath the jargon, it points to a simple question that matters a lot to your price, your deal terms, and what happens to your company after closing.

Say you own an HVAC business, a plumbing company, or another service firm built over decades. A buyer tells you, “We can pay more because of synergies.” What they usually mean is that your company is worth one amount by itself, but worth more in their hands because the combination could cut costs, lift sales, or improve the financial profile of the business. Sometimes that’s true. Sometimes it isn’t. And sometimes the promised synergy destroys value.

That last part is where many owners get blindsided. In small, relationship-driven businesses, the same “efficiencies” a buyer is excited about can weaken customer trust, unsettle employees, and break routines that hold the whole operation together. The practical definition of synergies in business isn’t just about upside. It’s also about understanding what can go wrong, especially when your name, your culture, and your reputation are part of what a buyer is buying.

A buyer sits across from you and says, “Your business is attractive because of the synergies.” If you’ve spent your life running crews, serving customers, and making payroll, that sentence can feel slippery. You know what a service agreement is. You know what gross margin is. “Synergy” can sound like something that only exists in a spreadsheet.

In plain English, it usually means this: your business may be more valuable to a particular buyer than it is on a standalone basis. Not because the buyer is generous. Because they believe the two companies together can perform better than each one operating alone.

That can show up in ordinary ways. A larger acquirer might fold your bookkeeping into its existing back office. It might negotiate better supplier terms because it buys more units. It might sell your maintenance plan to customers in a neighboring market where you’ve never had a presence. Those are all synergy claims.

Most owners don’t need a textbook definition first. They need to know whether the buyer’s “extra value” is real, reachable, and worth sharing.

The important thing is to hear the word the way an advisor hears it. Not as a compliment, and not as magic. Hear it as a proposal. The buyer is saying, “We think this combination creates additional value.” Your next thought should be, “Show me how.”

That’s where the definition of synergies in business becomes useful. Once you strip away the pitch language, you can sort synergy into a few practical buckets, ask better questions, and spot the difference between savings that are likely and promises that depend on everything going perfectly.

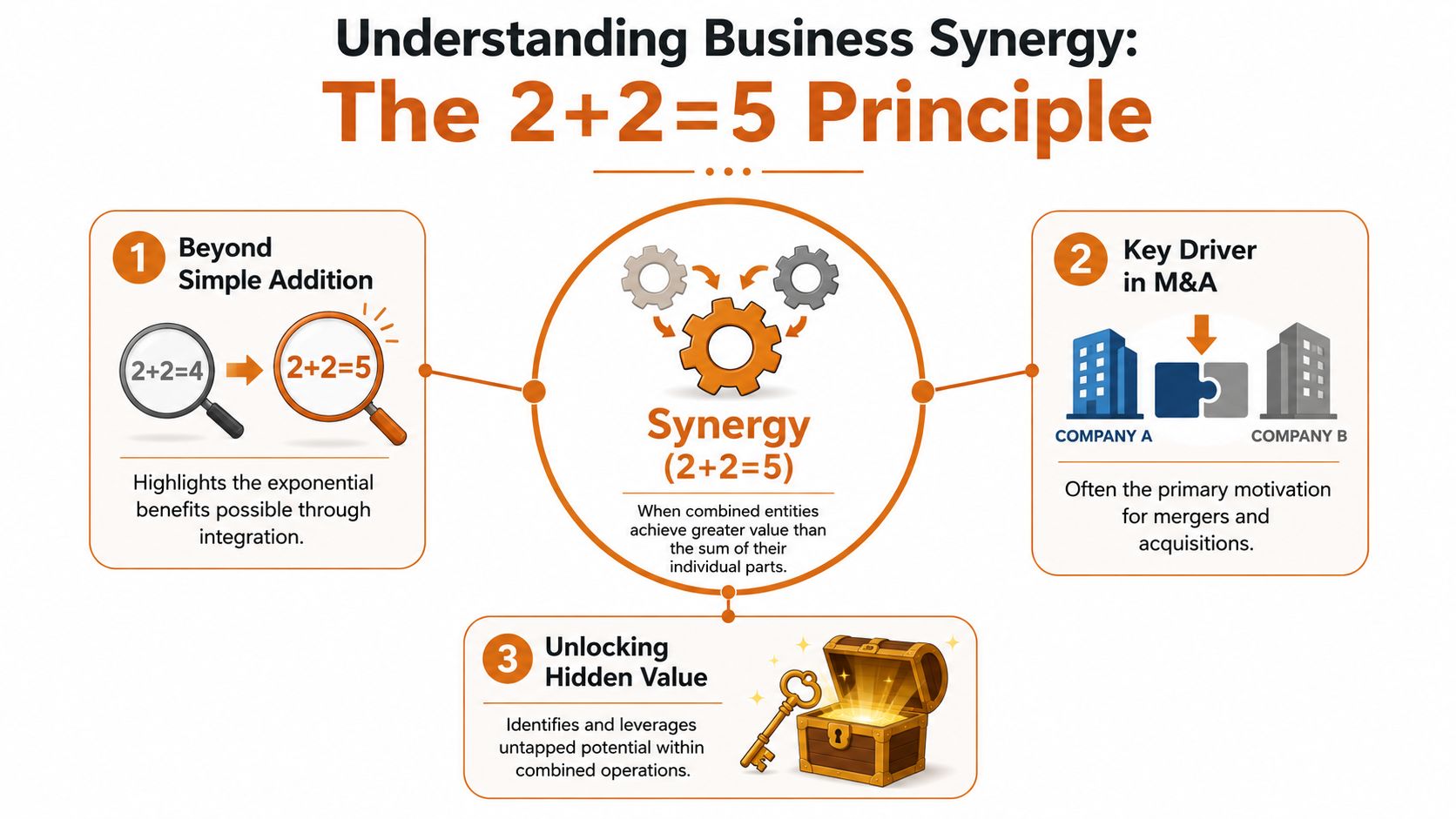

The oldest shorthand for synergy is “2 + 2 = 5.” It sounds silly at first, but it captures the core idea better than most boardroom language. Two businesses come together, and the combined result is greater than the simple sum of the two separate companies.

That idea sits at the center of M&A. According to BCG’s discussion of M&A synergies and value, synergy is the tangible expected improvement in earnings when two businesses merge, and financially it’s measured as the present value of incremental after-tax cash flows generated by the combination, net of integration costs, dis-synergies, required investment, and execution risk.

Foundational definition: Synergy is the additional value created by combining two businesses that would not exist if each company kept operating on its own.

A buyer rarely pays a premium just because they like your company. They pay more when they believe the combination creates value they can’t get otherwise. That’s the economic reason synergy matters. It explains why one buyer may offer more than another for the exact same business.

A simple analogy helps. Think of two neighboring service companies. Each has dispatch, accounting, advertising, trucks, and technicians. Separately, both carry those costs. Together, they may only need one accounting team, one office lease, one software stack, and one purchasing relationship for key equipment. If that works, the combined business throws off more cash.

When people use the term, they’re usually talking about one of three forms:

Those categories matter because they are not equally reliable. Some are visible and easier to test. Others are more speculative and depend on execution, timing, and people behaving the way the model assumes they will.

That’s why owners get confused when a buyer says “there’s a lot of synergy here.” It may sound like one neat concept, but in practice it’s several different claims bundled together. Until you unpack those claims, you don’t know whether you’re hearing a realistic value case or a hopeful story.

The standard definition of synergies in business usually breaks them into cost, revenue, and financial synergies. Financial Edge’s overview of synergies describes those three categories as fundamental to valuation and to the basic idea of businesses “working together.”

This is the easiest one to grasp. Cost synergy means the merged company can remove duplicate expenses. Two businesses become one platform, so some costs no longer need to exist twice.

In a trade business, that could look like:

Owners tend to understand this quickly because it feels tangible. You can point to an office, a lease, a software subscription, or a role and say, “That’s duplicated.”

Revenue synergy means the combined business can generate sales that neither company could easily generate alone. Buyers discuss aspects such as cross-selling, broader market reach, and complementary services.

A practical example: a plumbing company acquires an HVAC business. The combined company may now offer both services to the same homeowner base. That opens the door to maintenance plans, system upgrades, or emergency service calls across both disciplines.

This category sounds exciting because it points to growth, not just cuts. It’s also where projections can drift into optimism. Cross-selling looks obvious on paper. In real life, it depends on sales training, customer trust, systems integration, technician coordination, and brand consistency.

Financial synergy is less visible to day-to-day operators but still matters in deals. It refers to value created by improving the financial profile of the combined entity, such as lower cost of capital or better tax positioning.

For a larger buyer, your business may fit into a capital structure that gives the combined company more flexibility. Or the acquirer may be able to finance operations more efficiently than you could as a standalone owner-managed firm.

Here’s the short version:

| Type | Plain meaning | Typical owner reaction |

|---|---|---|

| Cost | “We can spend less together” | Usually easiest to believe |

| Revenue | “We can sell more together” | Often sounds good, but needs proof |

| Financial | “We can structure the business better together” | Real, but harder to see from the shop floor |

Revenue synergy isn’t fake. It’s just less automatic than buyers often make it sound.

If you remember one thing, remember this: not all synergy claims deserve equal weight. Owners should treat cost synergies as more concrete, and treat revenue and financial synergies as claims that need sharper questioning.

Synergy becomes important the moment a buyer turns a strategic idea into a price. At this point, the conversation moves from “we like your business” to “here’s what we’ll pay.”

In M&A, synergy is valued as the present value of incremental after-tax cash flows from the combination, net of costs and risks. StocksMantra’s example of synergy valuation gives a simple illustration: if Firm A is worth $500 million, Firm B is worth $75 million, and the merged entity is worth $625 million, the $50 million difference is the synergy value.

Buyers and lenders don’t treat every projected benefit the same way. Cost savings usually get more credibility because they are easier to identify and measure. If two companies will clearly eliminate one office, one finance system, or one duplicated role, that’s easier to underwrite.

Revenue growth is a tougher sell. A forecast that says “we’ll cross-sell to each other’s customers” may be plausible, but it rests on more assumptions. Customers may not buy. Employees may not execute. The systems may not support the plan. That’s why cost synergies are often referred to as hard synergies, while the rest are softer and less certain.

A buyer may use synergy to justify paying above your standalone value. But that doesn’t mean you should accept every dollar of claimed upside as if it already exists. Some of that value belongs to the buyer because they’re taking on the integration work and the risk that the plan fails.

A useful way to think about it is this:

This is also where owners often confuse synergy with goodwill. They overlap in conversations but they are not the same thing. If you want a cleaner distinction, this plain-language guide to the definition of goodwill in business helps separate buyer-specific value from broader intangible value.

A synergy claim only matters if someone can explain who will create it, what it will cost, and how long it will take.

That sentence sounds simple, but it cuts through a lot of noise. If a buyer can’t answer those three points clearly, the number probably deserves a discount in your mind.

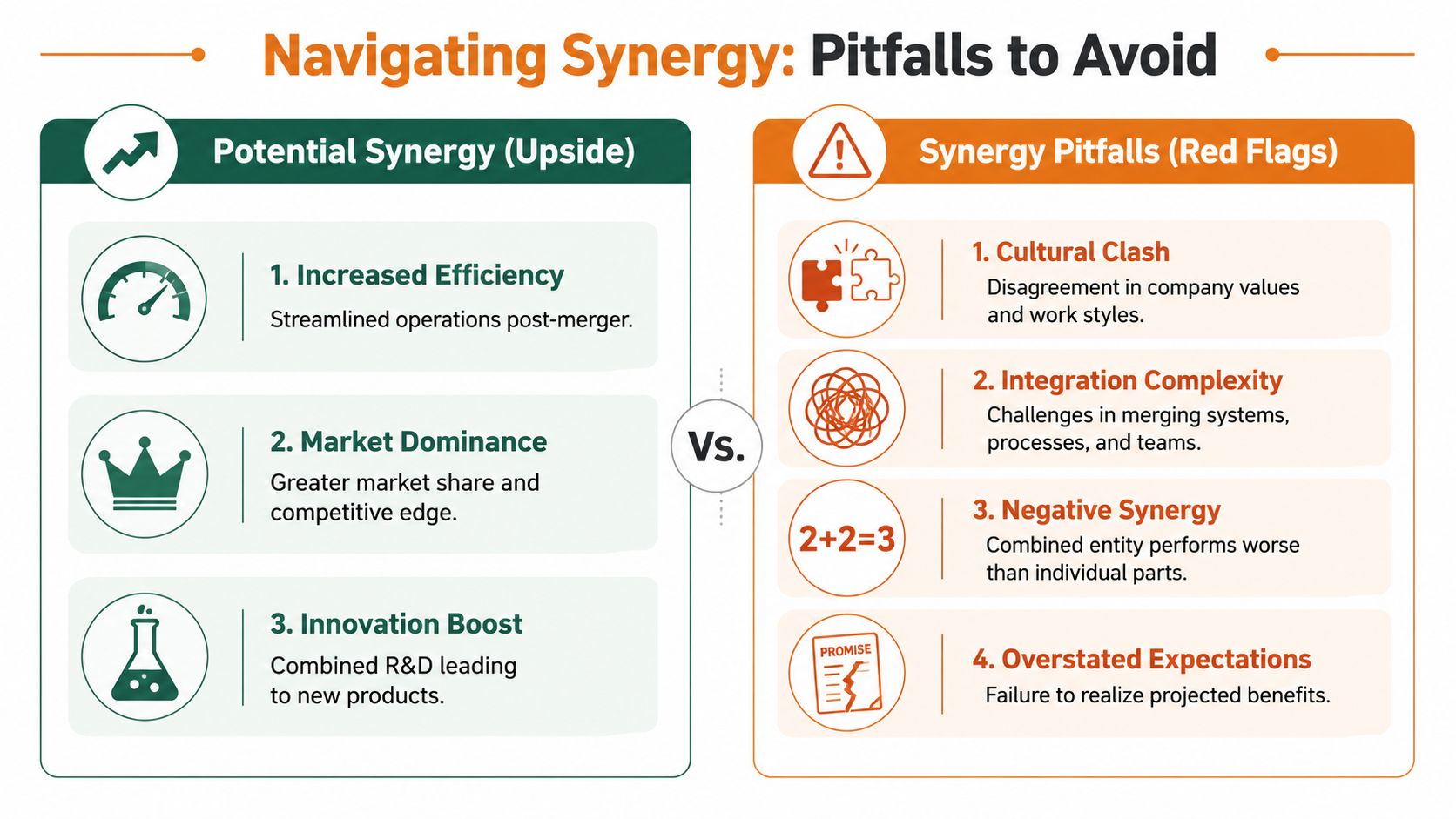

Most synergy talk focuses on upside. Owners need the other half of the picture. Synergy can fail, and when it fails in a people-driven company, the damage often starts in places that don’t show up immediately in the model.

Stratechi’s discussion of synergies notes that up to 73% of M&A deals in the U.S. fail to realize their projected synergies, often because of cultural misalignment. That’s especially relevant in owner-operated trades, where the company’s value may depend heavily on personal relationships and trust.

Negative synergy is the uncomfortable version of the same idea. Instead of 2+2=5, the combination behaves more like 2+2=3. The merged business performs worse because integration weakens what made each company work in the first place.

That can happen when:

This matters more in a local service company than in a large public company with a distant customer base. In a plumbing, HVAC, electrical, or route-based business, value is often tied to repeat customers, referral patterns, and the credibility of the owner. Those things don’t transfer neatly in a spreadsheet.

That’s why “efficiency” should never be accepted at face value. Sometimes the exact actions a buyer calls synergy are the actions that reduce retention.

A few practical red flags deserve extra attention:

Negative synergy doesn’t always show up as a dramatic collapse. Sometimes it arrives as a slow leak. A few employees leave. A few customers drift. Response times lengthen. The buyer still says the deal is “on track,” but the original value case starts fading.

You don’t need to become a deal modeler to handle synergy well. You do need a disciplined way to separate what is real, what is possible, and what is buyer optimism.

Start with your own business before you react to the buyer’s story. Write down the value drivers that are already present and transferable.

Focus on specifics such as:

This isn’t just prep work. It changes the conversation. Instead of letting the buyer define all synergy, you show which parts of the value are already embedded in the business and which parts depend on preserving what you’ve built.

When a buyer says they can “create value,” ask them to get concrete. Not adversarial. Just concrete.

Use questions like these:

If part of the purchase price depends on future results, be especially careful. In some deals, mechanisms like seller financing or contingent payments can shift integration risk back onto the seller. That doesn’t make them bad tools. It just means you should know when “shared upside” really means “you’re helping fund our synergy thesis.”

Owners get into trouble when they negotiate price without negotiating the assumptions behind the price.

That’s the point where experienced advisors save real money.

The definition of synergies in business isn’t only for third-party sales. It also matters in succession, especially when a child or relative is taking over. In those situations, some of the biggest synergies are soft and cultural.

Ideals VDR’s article on synergy concepts and examples cites a 2024 PwC study finding that 68% of family business transitions fail due to unmeasured cultural synergy gaps, not financial ones. It also notes that for long-tenured owners, intangible synergies such as reputation and loyalty can represent 30-40% of exit value.

That should sound familiar to any owner whose business runs on trust.

A simple framework helps:

| Soft synergy | What to document | Why it matters |

|---|---|---|

| Reputation | Key referral sources, community ties, repeat customer patterns | Shows what the family successor is inheriting |

| Loyalty | Employee tenure, informal leaders, service habits | Helps identify what must be preserved |

| Decision speed | How the business handles exceptions and customer issues | Reveals culture that may not show in financials |

Here’s a useful video primer if you want another plain-English perspective on valuing what a business is really made of:

When families ignore these soft synergies, they often treat the transition as a tax and legal exercise only. It isn’t. It’s also a transfer of trust, authority, and operating rhythm. Those factors don’t sit neatly in a traditional model, but they have real economic consequences.

It depends on the type and on execution. Cost synergies usually show up sooner because they often involve identifiable overlap, like facilities or back-office functions. Revenue synergies usually take longer because they depend on customers, sales execution, and integration going well.

That depends on the purchase agreement and the deal structure. If the buyer pays cash at closing, the buyer usually bears most of the risk that their synergy thesis doesn’t come through. If part of your payout depends on future performance, such as an earnout or seller-backed structure, you may still carry some of that risk indirectly.

Not exactly. Economies of scale are one possible source of synergy, usually on the cost side. Synergy is the broader concept. It includes cost savings, potential revenue gains, and financial improvements created by combining businesses. So economies of scale can be part of synergy, but they aren’t the whole idea.

If you’re weighing a sale, succession plan, valuation, or deal structure question, The Owner’s Shortlist helps long-tenured owners find vetted specialists in valuation, taxes, legal matters, financing, and family transition planning, along with practical guides that explain the process in plain English before you start making decisions.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

Get a clear definition of goodwill in business for owners. Explore personal vs. enterprise goodwill, valuation, sale price & tax impact.

July 8, 2026

Learn how to value a small business with our practical guide for owner-operators. We cover valuation methods, SDE calculations, and how to prepare for a sale.

July 6, 2026

A 3-step small business valuation any trades owner can run in 20 minutes with last year's tax return. Get a ballpark before you talk to anyone.

June 14, 2026

A 1x difference in your multiple can mean $500,000 more or less in your pocket. Here's how buyers calculate what your business is worth, in plain numbers.

May 22, 2026