How Can I Open a Franchise: Your 2026 Roadmap to Success

Learn how can i open a franchise in 2026. Get expert tips, a step-by-step guide, and essential resources to successfully start your business journey this year.

July 10, 2026

July 14, 2026

You may be in this spot right now. The business is solid, the phones ring, the crews know what they’re doing, and a real buyer wants it. But the bank won’t finance the full purchase price.

That happens all the time in owner-operated business sales. A buyer can be capable, experienced, and motivated, yet still come up short with conventional lending. For a plumbing shop, HVAC company, electrical contractor, or route-based service business, that gap often decides whether you get a clean deal or a stalled one.

Seller financing becomes useful. Not as a desperate fallback, but as a tool. The key is understanding that financing the sale of a going concern is different from financing a house. The collateral is different. The risk is different. The note has to survive real operating problems, not just a missed mortgage payment.

A long-time owner often assumes the sale process is simple. Find a buyer, let the bank underwrite the deal, collect the money, and move on. In practice, that clean version breaks down fast.

A strong service manager may want to buy your company but lack enough cash. A competitor may love your customer base but not get comfortable terms from its lender. A family successor may know the business inside out and still fail a bank’s approval process. None of that means the buyer is weak. It means lenders have boxes, and owner-operated businesses don’t always fit neatly inside them.

That’s why seller financing keeps showing up in real deals. It bridges the gap between what the buyer can fund and what you’re willing to accept. In business sales, that bridge needs to be built with care.

Most seller financing articles talk like you’re selling a house. You’re not. You’re transferring a machine that has to keep producing cash after closing.

That difference matters. Guidance on business seller financing from LendingTree notes that most content focuses on residential real estate, even though owner-operated business transitions bring different risks around default, subordination, and balloon payments. In a business sale, the seller often needs to retain a mortgage on working assets while the buyer takes over operating risk.

For a home services company, that can mean the note depends on trucks staying on the road, dispatch staying organized, key techs staying employed, and recurring service agreements staying intact. If those pieces wobble, your note can wobble with them.

A house doesn’t lose value because a service manager quits or because renewals slip. A business can.

The most common mistake I see is treating bank approval as the same thing as buyer quality. It isn’t. Plenty of capable buyers can run the company and still need help getting the deal over the line.

That doesn’t mean you should play banker casually. It means you should look at seller financing as one possible part of a larger structure, with protections that fit a going concern.

Generic lists usually stop at broad points like “more buyers” and “risk of default.” True, but incomplete.

For a business owner, the essential questions are harder:

Those are business sale questions, not residential real estate questions. If you own a company with equipment, employees, and recurring customer revenue, the structure matters as much as the price.

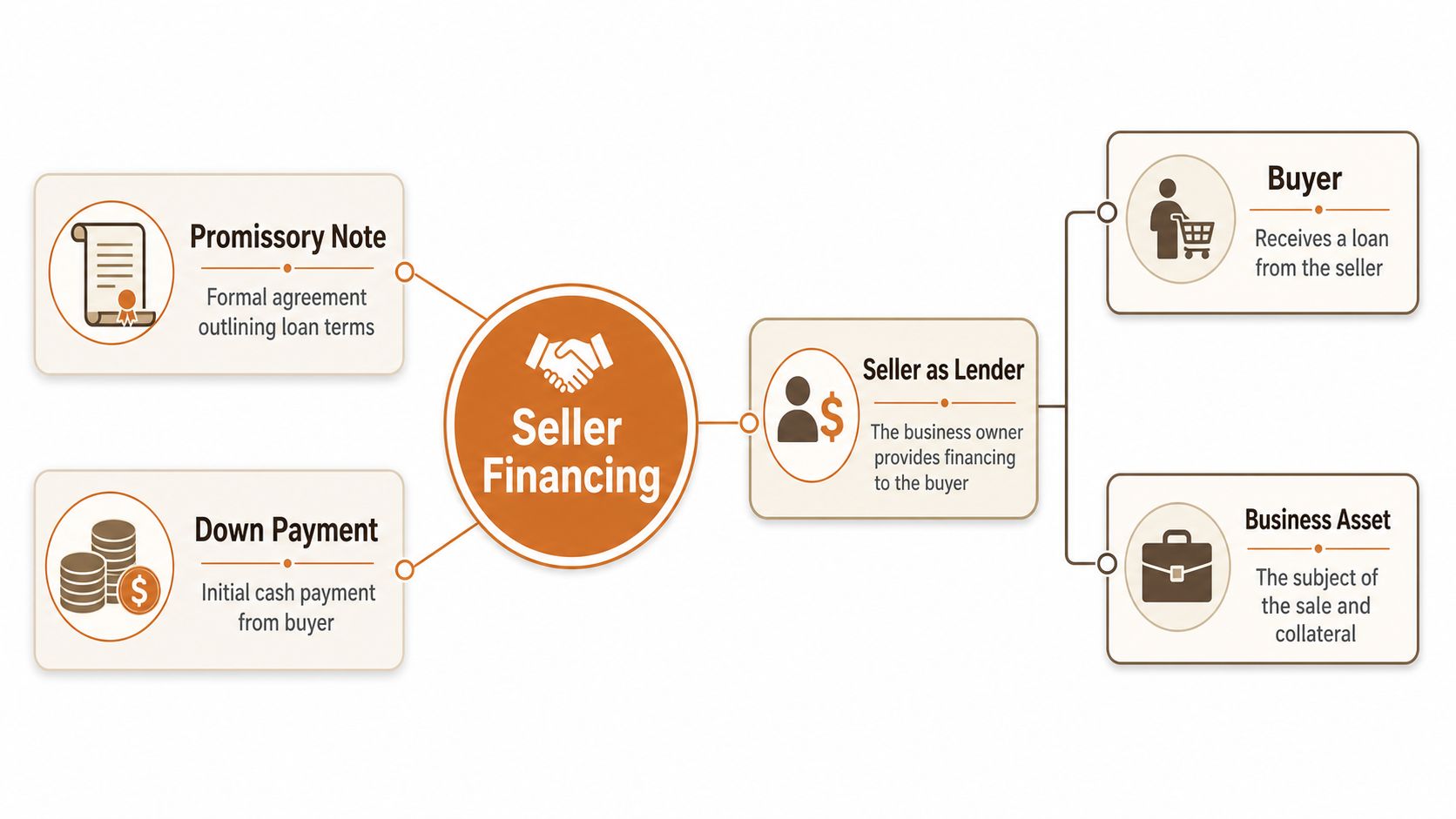

Seller financing in a business sale means you accept part of the purchase price over time instead of taking all proceeds at closing. Put plainly, you become the lender for part of your own sale.

The buyer usually brings some cash, outside financing, or both. You carry the remaining agreed portion under a promissory note. That note lays out the repayment terms, and the security documents say what happens if the buyer defaults.

If you want a simpler primer on the mechanics, this overview of how seller financing works is a helpful companion before you start negotiating terms.

Imagine selling a service fleet but agreeing that part of the price gets paid from future operations. You’ve transferred ownership, but you still have financial exposure until the note is paid off.

That’s why seller financing isn’t just “take payments later.” It’s credit underwriting. You need to assess whether this buyer can operate the company well enough to pay you, while also protecting your position if they can’t.

The basic flow usually looks like this:

The documents matter more than the handshake. At minimum, most seller-financed business deals revolve around a few core pieces:

Practical rule: If the note isn’t tied to identifiable assets and clear remedies, you don’t have much protection. You have hope.

In trade businesses, collateral can include the vehicle fleet, tools, customer lists, and recurring service agreements. Those service agreements deserve special attention. If your company’s value rests on renewing memberships or maintenance plans, the note should recognize that those contracts aren’t side items. They’re part of what makes repayment possible.

Seller financing pros and cons look different when you’re selling a live business instead of a static asset. The upside is real. So is the risk.

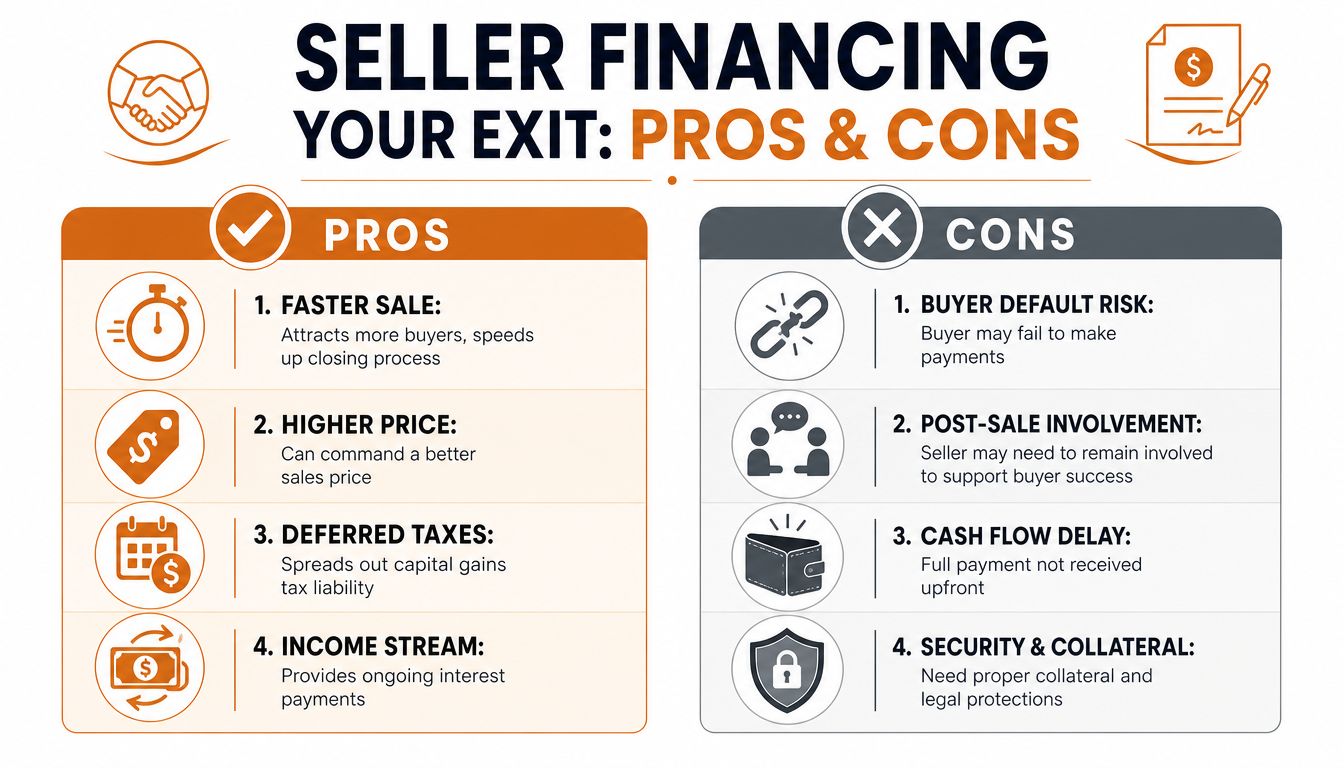

Start with the upside. A key technical advantage is pricing power. According to this seller financing analysis on YouTube, seller financing can support a sale price often 3 to 5 percent above comparable cash or bank-financed deals because it expands the buyer pool. The same source notes the trade-off. Sellers often receive full proceeds over a 3 to 7 year term rather than all at once.

The first benefit is straightforward. You can sell to a broader set of buyers.

That matters in owner-operated companies because many good buyers are operationally strong but undercapitalized. A lead installer, service manager, or small strategic buyer may know how to run the business but still need help closing the capital stack. Seller financing can make that buyer viable without forcing you to slash the asking price.

A second benefit is alignment. When the seller carries part of the note, the buyer often reads that as confidence in the business. That can keep negotiations moving when a lender is hesitant.

There can also be tax planning implications in some structures. This article on what an installment sale is is worth reading before you decide how much paper to carry.

Later in the process, some owners also like the idea of an ongoing income stream from note payments. For the right seller, that can feel similar to replacing owner distributions with scheduled receipts.

To add a practical overview, this short video is useful:

The main con is not abstract risk. It’s default risk tied to operating performance.

If the buyer runs the company poorly, your note can go bad even if the business looked healthy at closing. In a trade business, that decline can start subtly. Tech turnover rises. Call conversion drops. Renewal discipline slips. Gross margin gets sloppy. By the time missed payments show up, the business may already be worth less than when you sold it.

Here’s the side-by-side view:

| Issue | Potential upside | Potential downside |

|---|---|---|

| Buyer pool | More qualified operators can bid | More marginal buyers may ask for terms |

| Sale price | Seller financing can support a premium price | A higher price means little if collection fails |

| Cash at closing | Deal gets done when bank debt falls short | You delay part of your payout |

| Post-closing economics | Interest can add return on the financed portion | You stay exposed to business performance |

Another con is emotional. Owners think they’re done, but a weak structure can pull them back into the business. If the buyer struggles, you may get dragged into disputes over records, collateral, or missed covenants.

That’s why seller financing works best when the note is treated like a credit instrument, not a gesture of goodwill.

A seller-financed deal only works if the paper is worth something. That comes down to structure, not optimism.

In business sales, a commonly recommended approach is to keep seller financing limited to 20 to 30 percent of the total purchase price, protect it with first-position liens, and charge market interest rates defined as prime rate plus 2%. Guidance for business-sale seller financing also recommends performance covenants tied to EBITDA so the buyer has to preserve operating profitability during repayment, as explained in George & Company’s discussion of seller-financed business sale pros and cons.

If you’re going to carry paper, focus on these five levers.

The rate needs to reflect risk and delayed liquidity. You’re not a charity, and you’re not a bank with a diversified loan book. If you carry a note, the pricing should compensate you for the fact that your sale proceeds arrive over time and depend on one buyer operating one business correctly.

Many owners get into trouble by financing too much. A smaller seller note forces the buyer and any senior lender to carry more of the burden. It also protects your capital if the business stumbles after closing.

First-position security matters. If your note is secured by the business assets, but another lender controls the meaningful collateral, your remedies can become weak in a hurry.

That’s especially important in trade businesses where hard assets and customer relationships both matter. A first-position claim on vehicles, equipment, receivables, and other identifiable assets gives you a better recovery path than vague language about “the business” as collateral.

Performance covenants are not overkill. They’re guardrails.

If the buyer strips cash out, stops maintaining equipment, lets insurance lapse, or allows operating performance to deteriorate, you need a contractual way to step in before the note is in full default. EBITDA-based covenants are one tool. Reporting requirements, minimum working capital standards, and limits on owner distributions can also help.

The seller who says “I trust the buyer” but skips covenants is lending against personality instead of performance.

A personal guarantee changes the conversation. It gives the buyer skin in the game beyond the newly acquired company itself.

Without one, a buyer may be tempted to treat the acquired entity as the only thing at risk. With one, the buyer has stronger personal incentive to protect the business and keep the note current.

Take an HVAC company with maintenance agreements, a branded vehicle fleet, dispatch software, and a recognizable local name. The buyer purchases the company and plans to repay part of the price from future cash flow.

A protected structure usually asks practical questions like these:

The costly mistake many business owners make is focusing on sale price first and paper quality second. That’s backwards. A strong note can make a fair deal worthwhile. A weak note can turn a high headline price into a collection problem.

If you’re considering seller financing, treat this like a lender would. Better yet, be stricter than a lender, because banks don’t also have their retirement proceeds tied to one note.

For screening discipline, this guide on how to check out a buyer is worth reviewing before you discuss terms.

Use this as a working checklist in early negotiations:

Once you move past buyer quality, the paperwork needs to carry the load.

A seller note should be easy to explain in plain English. If nobody at the table can explain the remedies, the documents are not ready.

This checklist won’t eliminate risk. It does force the hard conversations early, while you still have an advantage.

Seller financing is a fit when the business is stable, the buyer is credible, and you don’t need every dollar on day one. It’s a poor fit when any one of those three breaks.

It tends to work well in companies with predictable operations and visible revenue quality. Trade businesses with repeat customers, maintenance relationships, and steady demand often fit better than companies that lurch from project to project.

A good buyer profile also matters. The best seller-financed deals often involve a buyer who understands the industry, has enough capital to matter, but can’t quite close the full gap with bank debt alone. In that situation, seller financing acts like a bridge, not a crutch.

Strong alignment helps too:

Avoid seller financing if you need full liquidity for retirement, another investment, or estate planning moves that can’t wait. Delayed proceeds are not a small detail. They change your personal balance sheet.

It’s also dangerous in a shaky business. If revenue is erratic, margins are thin, or the company needs a turnaround, you may be handing the buyer a problem and then betting your unpaid proceeds on their ability to fix it.

Walk carefully if the buyer has no track record in the industry. A person can be smart, honest, and well-meaning, then still fail because they’ve never managed technicians, job costing, call volume, or recurring customer retention.

A simple test helps. If the business misses plan for six months after closing, do you still like your position as lender? If the answer is no, the structure probably isn’t strong enough.

Before you sit down with an M&A advisor, transaction attorney, or tax specialist, it helps to have a plain-language term sheet in mind. Not a legal document. A discussion draft.

A practical outline might include:

Current rules matter. The tax and regulatory treatment of a seller-financed deal can change based on structure, frequency, and payment design. The National Association of Realtors notes that a key issue for specialists is how current IRS and banking rules, including 2024 updates to the Ability-to-Repay rule, affect a specific transaction. That same NAR discussion of seller financing also warns that misstructuring items such as interest-only periods or revenue-sharing balloons can create unintended liabilities or disrupt favorable tax treatment.

Bring questions like these to your first specialist call:

A seller-financed deal can be smart. It can also be expensive in all the wrong ways if the note, collateral, and tax treatment are handled casually.

If you’re weighing seller financing and want help finding the right advisor before you commit, The Owner’s Shortlist gives long-tenured business owners a practical place to start. It connects owners with vetted specialists in valuation, taxes, legal matters, financing, and succession, and its plain-language guides help you ask better questions before the first meeting.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

Learn how can i open a franchise in 2026. Get expert tips, a step-by-step guide, and essential resources to successfully start your business journey this year.

July 10, 2026

A seller's note means you finance part of your own sale. Learn how they're structured, how they differ from earnouts, and what to negotiate before signing.

May 13, 2026

Seller financing means you get paid over time instead of all at once. Here's how it works, what it costs you, and when it makes sense.

April 10, 2026