Exit Planning for Business Owners: Your 2026 Guide

A plain-language guide to exit planning for business owners. Learn to assess valuation, navigate taxes, build a timeline, and choose the right specialists.

July 17, 2026

July 18, 2026

You can have a company that would command a strong valuation in a buyer meeting and still feel uneasy writing a personal check for a major tax payment, a real estate purchase, or a family transfer. That tension is common for founders and owner-operators. On paper, you’re wealthy. In practice, most of your net worth sits inside one illiquid asset that doesn’t pay your personal bills unless you sell, refinance, or distribute cash.

That’s why wealth planning for high net worth individuals looks different when the individual is also the business. Generic advice assumes a liquid portfolio. Business owners usually face a harder mix of concentration risk, tax exposure, family pressure, and timing decisions that can’t be reversed once a sale process starts. The best plans solve for cash flow, control, and optionality long before an exit.

A familiar scenario goes like this. The owner has spent years building a strong company, employs good people, and gets unsolicited buyer calls. Their accountant says the business is valuable. Their attorney says they should update estate documents. Yet the owner still hesitates before taking money out of the company, still worries about a downturn, and still knows that most of the family balance sheet depends on one operating business continuing to perform.

That’s the asset-rich, cash-poor paradox.

A lot of high-net-worth guidance misses this reality because it starts with marketable securities, not owner-operated companies. But concentrated business wealth creates its own planning problem. As Marshall Financial Group notes in its discussion of HNWI planning for concentrated owners, many owners hold over 10% of their wealth in a single operating company, and standard planning often skips the mechanics of accessing that wealth without triggering a major tax event or forcing a premature sale.

You don’t have a planning problem because you lack wealth. You have a planning problem because your wealth may be trapped inside the wrong wrapper at the wrong time.

That shows up in ordinary decisions. An owner wants to help a child buy a home, fund a trust, diversify into real estate, or make a strategic investment. The net worth is there. The liquidity isn’t. So the owner delays, borrows personally on unattractive terms, or takes oversized risk by leaving even more wealth concentrated in the business.

The practical mistake is treating personal wealth planning as something that happens after the exit. For business owners, it starts before the exit, because your personal balance sheet and your company capital structure are already tied together. If you don’t address that link early, you end up reacting under pressure. That’s when owners sell too soon, distribute cash inefficiently, or sign a deal structure that works for the buyer but not for the family.

Most failed plans don’t fail because the owner chose the wrong product. They fail because the owner never defined what the money is supposed to do. A business owner who wants to pass the company to a child needs a different structure from one who wants a third-party sale, a charitable legacy, or capital for a second act.

Before talking about trusts, tax elections, or alternative investments, answer four questions:

When owners do this well, the planning gets clearer fast. If your priority is family continuity, you may accept slower diversification in exchange for control and governance. If your priority is independence from the business, you’ll usually want earlier liquidity, tighter personal cash flow planning, and less tolerance for reinvesting excess capital back into the company.

A useful wealth plan for a founder usually balances four variables:

| Decision area | If you favor this | You often give up this |

|---|---|---|

| Growth | Reinvesting heavily in the business or alternatives | Liquidity and personal flexibility |

| Liquidity | Cash reserves, partial sale, or lower concentration | Some upside and some control |

| Control | Voting power and retained ownership | Tax efficiency and diversification |

| Legacy | Family transfer and long holding periods | Simplicity and sometimes harmony |

That trade-off is visible in how affluent investors now allocate capital. According to Long Angle’s 2026 benchmark research on high-net-worth asset allocation, high-net-worth investors have moved away from the old 60/40 model, with the average investable portfolio now at 57% public equities, 31% private and alternative assets, and 12% bonds and cash. For business owners, that shift matters because it reflects a broader acceptance of illiquidity when there’s a clear purpose behind it.

But there’s a big difference between choosing illiquidity and being trapped by it.

Practical rule: Illiquid assets should be held by design, not by default.

That’s where a written personal capital policy helps. It doesn’t need to be fancy. It should state how much liquidity the household needs, what percentage of wealth can remain tied to the business, what assets should be carved out for family or estate goals, and what would trigger a sale, recapitalization, or transfer discussion. Owners who put that in writing make better decisions because they stop treating every surplus dollar as business capital.

Wealth planning for high net worth individuals gets more effective when goals lead and tactics follow. Without that sequence, even smart strategies can pull in opposite directions.

Tax and estate planning gets real for business owners when the business starts to appreciate faster than the owner’s personal infrastructure. The documents may be outdated. The entity structure may have made sense years ago but not now. The owner may have plenty of enterprise value and very little preparation for what happens if they sell, die, become disabled, or want to transfer shares gradually.

For larger estates, timing matters. As WiserAdvisor explains in its review of planning rules under the updated 2025 OBBBA framework, the projected lifetime estate tax exemption is $15 million for individuals and $30 million for couples in 2026. Families above those projected levels face a compressed timeline if they want to use higher exemptions before any future reduction.

That doesn’t mean every owner should rush into aggressive gifting. It means the old habit of “we’ll deal with estate planning later” is risky. If your estate could exceed those projected thresholds, delay can cost flexibility. If your estate is below them, you may have more room to simplify and avoid overengineering.

Here’s the plain-English version of the tools owners hear about most often:

These aren’t products to buy because someone mentioned them at a dinner. They’re structures. The right question isn’t “Should I have a GRAT?” It’s “What problem am I solving, and what asset belongs in that structure?”

A business owner preparing for a likely sale might use a trust to move future appreciation out of the estate before buyer interest accelerates. Another owner might use life insurance inside an ILIT because one child will run the business and another won’t, and the family wants a non-business asset available for balance.

Here’s a useful explainer before those conversations get technical:

For business owners, tax planning isn’t separate from exit planning. It is exit planning.

A few moves tend to matter more than owners expect:

Long Angle’s discussion of high-net-worth strategies for business owners makes the broader point well. Owners need diversification into alternatives such as real estate or private equity, plus tax-loss harvesting and insurance planning, because concentration risk can turn a business problem into a family balance-sheet problem very quickly.

The wrong way to approach this is product first. The right way is transaction first. What event are you preparing for, what tax result are you trying to improve, and what control are you willing to give up to get there?

Trusts intimidate a lot of owners because the terminology sounds legalistic and the documents are long. The practical idea is much simpler. A trust is a way to separate ownership, control, benefit, and timing. That’s powerful when a large part of family wealth came from one company and you don’t want the next generation receiving assets outright with no structure.

Start with the basic distinction.

A revocable trust is mostly an administrative and continuity tool. It can help avoid probate, keep titles organized, and make transition easier if the owner becomes incapacitated. It usually doesn’t remove assets from the taxable estate.

An irrevocable trust is where tax planning, asset protection, and transfer control become more meaningful. Once assets are transferred, the owner generally gives up some flexibility. In return, the structure can offer stronger protection and better transfer outcomes.

A simple comparison helps:

| Trust type | Best use | Main limitation |

|---|---|---|

| Revocable | Probate avoidance, organization, incapacity planning | Limited estate tax benefit |

| Irrevocable | Asset protection, estate reduction, controlled transfer | Less flexibility after funding |

The easiest way to think about a trust is as a financial safe with a custom rulebook. The assets go inside the safe. The rulebook says who can access them, when, and for what purpose.

That matters for business families. Suppose an owner wants children to benefit from wealth but doesn’t want unrestricted distributions at a young age. A trust can permit distributions for education, a first home, health needs, or business opportunities, while protecting assets from a beneficiary’s creditors, lawsuits, or divorce risk depending on how the trust is drafted and administered.

A good trust doesn’t just transfer money. It transfers intent.

For family business owners, this is often as much a governance decision as a tax decision. If one child works in the company and another doesn’t, the trust can support fairness without forcing equal operational authority. If the owner wants family wealth to remain available for descendants but not become a source of constant requests, the trust can establish standards before emotions take over.

Owners also need to understand what trusts do not solve. A trust won’t fix weak communication, poor succession preparation, or a lack of liquidity. It is a wrapper, not a cure-all. The design has to match the family reality.

If you want a practical owner-focused overview of those issues, estate planning for business owners is a useful starting point. The key is to treat trusts as operating tools for family wealth, not just legal paperwork filed away after signing.

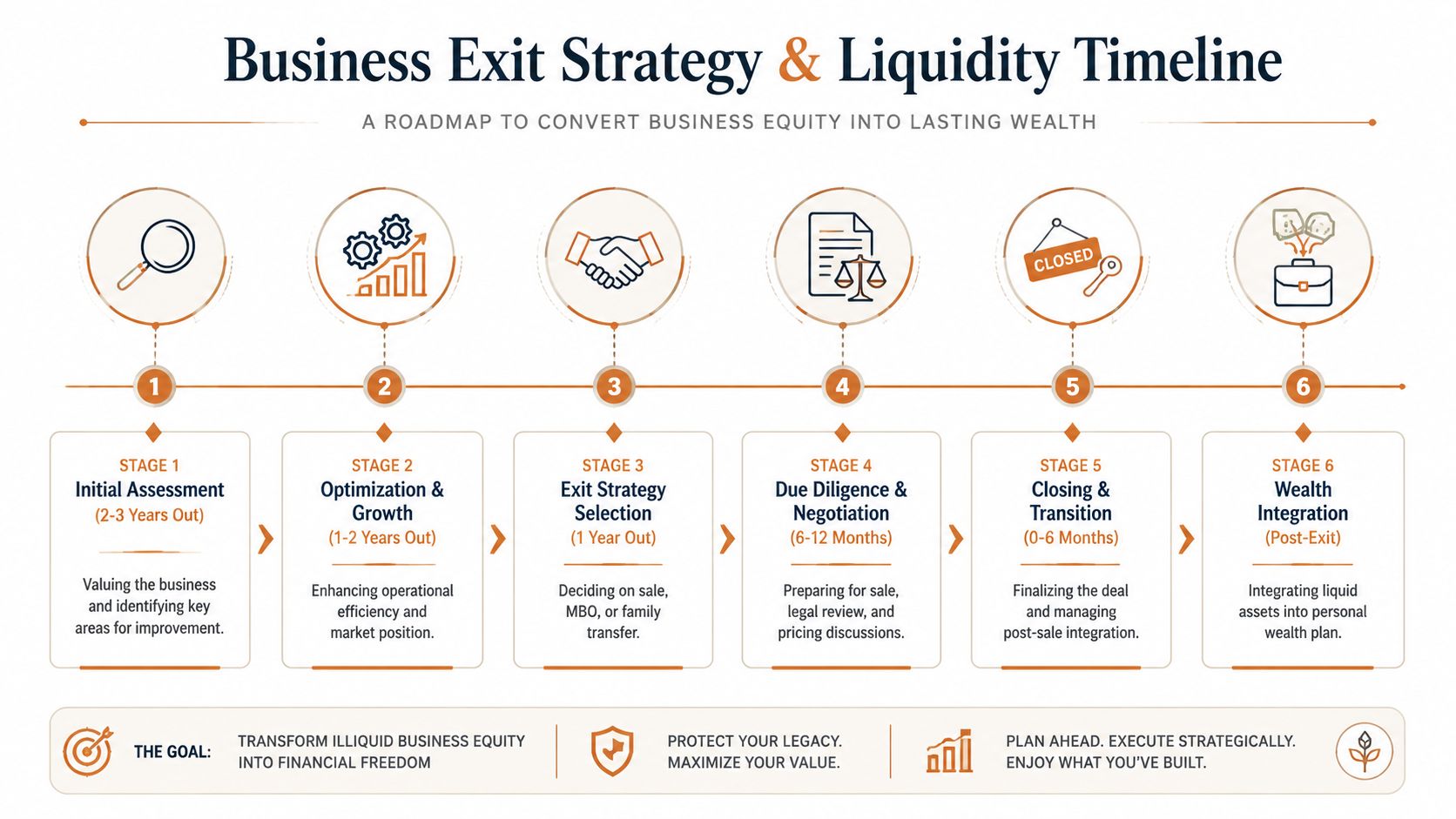

A founder’s biggest wealth problem is often not valuation. It’s conversion. How do you turn enterprise value into personal liquidity without creating a tax mess, weakening the company, or exiting before you’re ready?

That question deserves a separate plan because many owners wait until a buyer appears. By then, most of the good options have narrowed.

Not every owner needs or wants an immediate sale. Pre-exit liquidity can come from several directions, each with trade-offs.

The pre-exit liquidity decision usually comes down to one question. Are you trying to reduce pressure, or are you trying to leave? Those are different strategies. Owners get into trouble when they take “exit-like” actions to solve what is really a short-term liquidity issue.

The business side and personal side have to be built together. A sale process that maximizes headline value but ignores taxes, estate positioning, and post-close cash needs can leave the owner disappointed with the part that matters most, which is what the family keeps and can use.

A practical exit plan usually includes these elements:

Decision filter: If a liquidity move makes the company weaker, raises personal stress, and doesn’t improve long-term options, it probably isn’t the right move.

Diversification belongs in this conversation too. Long Angle notes in its article on high-net-worth business-owner strategy that diversifying into alternatives such as real estate or private equity, combined with tax-loss harvesting and umbrella insurance, is an important safeguard against concentration and forced liquidation risk. For many owners, diversification shouldn’t start after the sale. It should begin before the sale, while options still exist.

Owners thinking seriously about a transaction should also review how to prepare your business for sale. Exit outcomes improve when preparation starts while you still have bargaining power, not after buyer momentum has taken over the timeline.

Owners who built companies from scratch often prefer to solve problems directly. That instinct helped build the business. It can hurt wealth planning. The issues are too interconnected for one generalist, and too costly for a fragmented group of specialists who never speak to each other.

The scale of intergenerational transfer alone makes that clear. According to the Charles Schwab high-net-worth investor survey findings, ultra-high-net-worth Americans are expected to transfer nearly $12 million per individual on average, and the complexity of that transfer points to the need for coordinated tax, legal, and estate expertise.

A good advisory team doesn’t mean more people than necessary. It means the right people with clear roles.

If you want a plain-language description of one of those roles, what an exit planning advisor does is worth reviewing.

The common mistake is hiring strong professionals in isolation. The lawyer drafts a trust. The CPA focuses on compliance. The investment advisor manages a portfolio. The deal advisor runs a process. Everyone is competent, but no one is responsible for the interactions between their recommendations.

That’s where owners lose money and flexibility.

For example, a gifting plan may make sense legally but fail because there isn’t enough liquidity to support the owner personally. A sale structure may look attractive commercially but create tax consequences the owner would have addressed differently with earlier planning. A portfolio shift may reduce market risk but leave the owner too exposed to a pending business event.

A coordinated team should be able to answer practical questions like:

| Question | Lead advisor | Who else should weigh in |

|---|---|---|

| Should shares be transferred before a sale process starts? | Estate attorney | CPA, wealth advisor, M&A advisor |

| How much cash should the owner take off the table now? | Wealth advisor | CPA, company leadership |

| Is rollover equity appropriate? | M&A advisor | Wealth advisor, CPA |

| How should family beneficiaries be treated fairly? | Estate attorney | Wealth advisor, owner, family governance participants |

The right team doesn’t just produce documents. They sequence decisions so one good move doesn’t break another.

That’s why wealth planning for high net worth individuals should be handled like a multidisciplinary operating project, especially when the wealth sits inside a private company. Owners don’t need more opinions. They need orchestration.

The first meeting is better when the owner arrives with facts, not just worries. Preparation saves time, sharpens recommendations, and helps the advisor distinguish between a liquidity issue, a tax issue, a governance issue, and an exit issue. Often it’s some combination of all four.

Bring the materials that show both the household balance sheet and the business reality.

If something is missing, don’t delay the meeting forever. Bring what you have and identify the gaps. Good planning starts with an honest inventory, not a perfect binder.

The advisor can’t set priorities until you do. Write down your answers in plain language.

A short self-assessment helps too:

Go into the first meeting ready to discuss trade-offs, not just goals. Advisors can work with imperfect data. They can’t work with vague priorities.

The best first meeting ends with a sequence. What needs immediate attention, what can wait, and who needs to be added to the table. That sequence is where planning becomes useful.

If you’re sorting through liquidity, exit timing, taxes, estate structure, or succession questions, The Owner’s Shortlist is a practical place to start. It connects business owners with vetted specialists across valuation, taxes, legal and estate, financing, succession, and related decisions, with plain-language guides that help you understand your options before you hire anyone.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

A plain-language guide to exit planning for business owners. Learn to assess valuation, navigate taxes, build a timeline, and choose the right specialists.

July 17, 2026

Discover how to make selling business to employees a success in 2026. Our guide covers ESOPs, direct sales, valuation, tax, financing, and a step-by-step

July 12, 2026

Discover what is financial due diligence & its critical role when selling your business. Our 2026 guide covers the process, red flags, and prep tips for owners.

July 7, 2026

Planning to sell to your best employees? Here's why it often fails, and how an ESOP solves the financing problem while giving all your crew a stake.

July 5, 2026