Wealth Planning for High Net Worth Individuals

Practical guide to wealth planning for high net worth individuals with business-tied wealth. Master 2026 tax, estate, and liquidity strategies for lasting

July 18, 2026

July 17, 2026

You built the company by solving problems that landed on your desk every day. Payroll. Customers. Equipment. Hiring. A lawsuit threat. A key employee who wanted to leave on a Friday afternoon. For years, “exit planning” probably sounded like something for private equity people in conference rooms, not for someone who still knows the alarm code and the names of the first ten customers.

Then something shifts.

Maybe you’re tired, but not burned out. Maybe you got an unsolicited call from a buyer and realized you had no idea what to ask. Maybe your spouse asked a simple question over dinner: “If you sold, what would we do next?” That question stops a lot of owners cold, because the business hasn’t just been a job. It’s been your identity, your routine, your scorecard, and in many cases the largest asset you own.

That’s why exit planning for business owners starts earlier, and deeper, than is commonly understood. It’s not just about running a sale process. It’s about deciding what kind of future you want, what risks you need to remove before someone else prices them against you, and what needs to change so the business can succeed without you at the center of everything.

The first real exit planning conversation usually isn’t about valuation. It’s about life after the handoff.

What’s next for you?

Not in a motivational-speaker sense. In a practical sense. Do you want a clean break, or would you hate that after three months? Do you want the highest price, or do you care more about protecting the team? Do you want your name to remain on the building, or would you trade that for certainty and speed?

Owners often wait to ask those questions because they feel indulgent. They aren’t. They shape every serious decision that follows. If you don’t know whether you want to stay involved, preserve a family legacy, or maximize immediate liquidity, you can’t judge whether an offer is good. You can only react to the number.

Most bad exits don’t fail because of one legal clause. They fail because the owner never got honest about what they wanted.

Exit planning for business owners is best understood as a control process. You’re creating options before circumstances create pressure. That may lead to a third-party sale, a transfer to family, a management buyout, or a slower transition that lets you step back in stages. The transaction structure matters, but it sits downstream from the personal decision.

There’s also a harder truth that long-tenured owners know in their bones. A company can become so tied to the owner that even imagining life without it feels disorienting. That emotional reality doesn’t make you less prepared. It makes you normal.

A useful starting exercise is simple:

If you can answer those questions with some clarity, you’re already farther along than many owners who have bankers, lawyers, and a draft letter of intent.

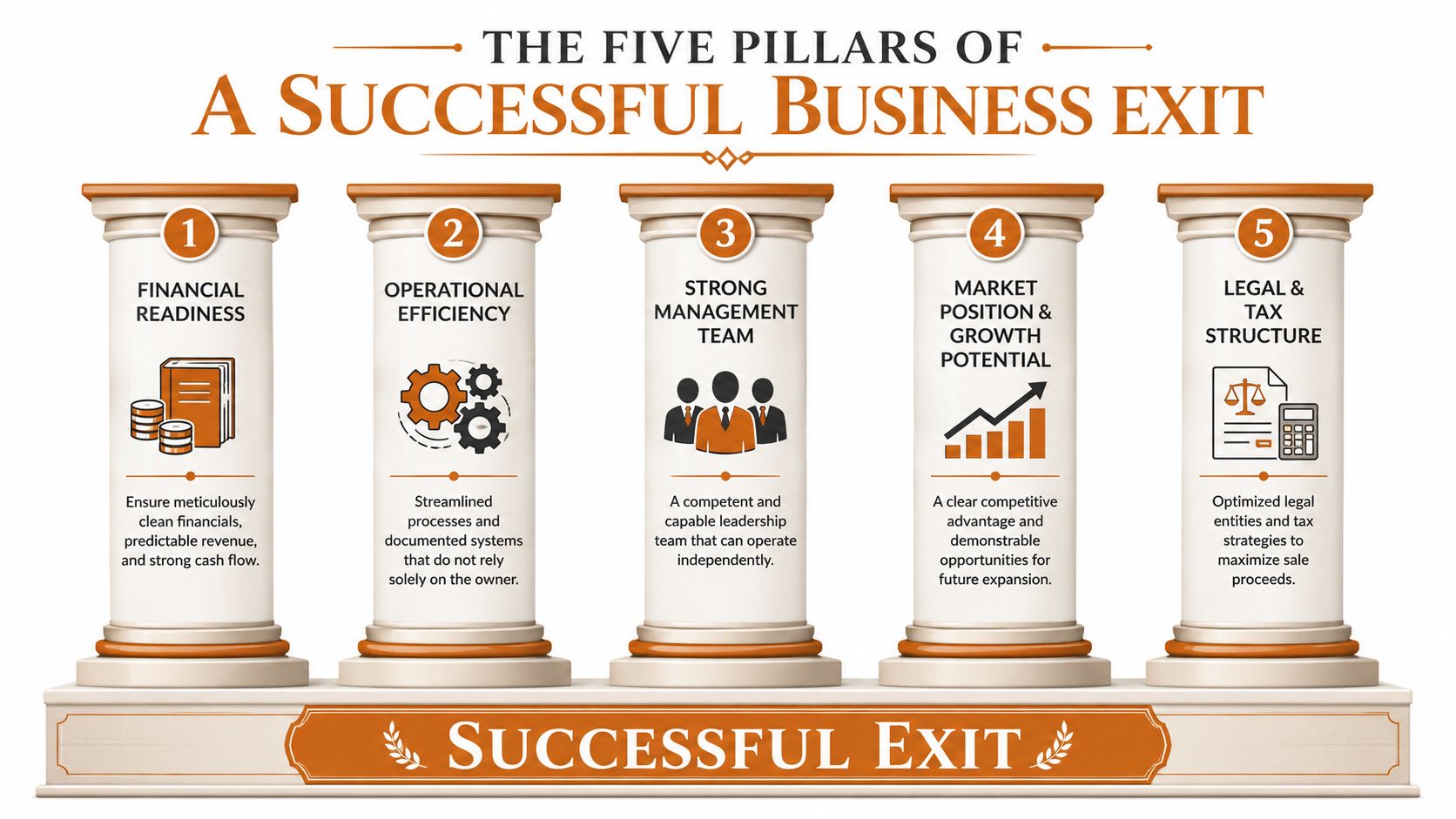

A successful exit rests on a handful of fundamentals. If one is weak, the whole structure starts wobbling when buyers push on it.

Most owners don’t fail for lack of effort. They fail because they focus on one pillar and assume the rest will sort themselves out. They clean up the financials but ignore owner dependence. They talk to tax advisors but never address leadership succession. They chase a headline valuation without defining what a good personal outcome looks like.

That’s why it helps to see the whole frame at once.

Financial readiness comes first because buyers trust numbers they can follow. Clean statements, coherent add-backs, predictable cash flow, and a credible view of future performance make diligence easier and negotiations less defensive.

Operational strength means the business runs through systems, not memory. If pricing lives in your head, vendor relationships depend on your cell phone, and key processes change based on who’s on shift, buyers see fragility. Owners often underestimate how much value sits inside repeatable execution.

A strong management team changes the feel of a deal. Buyers don’t just buy earnings. They buy the confidence that capable people can keep producing those earnings after the owner steps back.

Practical rule: If every important decision still routes through you, you don’t have a transferable business yet. You have a demanding job.

Market position and growth potential matter because buyers pay for what the business is likely to become, not just what it has been. A clear niche, strong customer retention, service depth, and visible expansion opportunities all strengthen the buyer’s case internally.

Legal and tax structure is the pillar owners often leave too late. Sloppy contracts, unresolved disputes, unclear ownership records, and weak tax planning can turn a strong offer into a frustrating outcome. Price is only part of the result. What you keep, and what risk stays attached to you, matters just as much.

Here’s the plain test:

| Pillar | Healthy sign | Warning sign |

|---|---|---|

| Financial readiness | Numbers are organized and defendable | Buyers will need to “normalize” too much |

| Operational strength | Processes are documented and repeatable | The business relies on owner memory |

| Management team | Leaders can run core functions independently | The owner is the decision bottleneck |

| Market position | Customers choose you for a clear reason | Growth depends on hustle alone |

| Legal and tax structure | Records and planning are in order | Issues surface late under pressure |

Owners who prepare across all five pillars usually gain something valuable before any deal closes. The company gets better now. It becomes easier to run, easier to delegate, and less vulnerable to your bad week, your vacation, or your eventual departure.

Most owners ask the valuation question as if it has one clean answer. It usually doesn’t.

Your business is worth what a qualified buyer can justify paying, under a specific structure, given the risks they see and the future they believe they can capture. That’s why two owners with similar revenue can get very different outcomes. One presents a stable, forecastable company with transferable systems. The other presents effort, history, and hope.

In practice, buyers tend to look at valuation through a few lenses. One is the familiar earnings multiple approach. Another is a cash flow view that asks what future cash the business is likely to produce and what risk sits around that projection. The technical term matters less than the practical point: buyers care about durable future earnings.

That’s where many owner-led businesses come up short. They have a budget for the next year, maybe. Buyers want a defendable forward view. A three-to-five-year financial forecast is especially important because it supports the DCF approach and helps reduce buyer skepticism about future performance, which can strengthen the case for a better multiple, as noted in PwC’s discussion of exit strategies and valuation preparation.

If you want a plain-English breakdown of how buyers and advisors think through valuation mechanics, this guide on how to value a small business is a useful companion.

Take an HVAC or plumbing company. An owner may say, “We’ve been around forever, customers trust us, and the phone keeps ringing.” That’s good, but it isn’t the same as contracted, recurring demand.

A business with maintenance agreements and service contracts gives a buyer something far more useful than optimism. It gives them visibility.

For trades businesses, that distinction can materially affect value. Businesses with more than 60% recurring revenue from service contracts can see valuation premiums of 15% to 25% over project-based peers, according to the analysis referenced in Ambition CFO’s exit planning discussion.

The lesson isn’t limited to the trades. Buyers like revenue that repeats without being re-sold from scratch every month. Contracted service, routine maintenance, subscription-style billing, and non-discretionary repeat demand all tend to reduce perceived risk.

Owners usually make one of three mistakes.

The cleanest valuation conversations happen when the owner can move from “I think it’s worth this” to “Here’s why a buyer can defend this number.”

If you want to raise value, work on the drivers a buyer can underwrite. Strengthen recurring revenue. Build a forecast you can explain line by line. Reduce surprises in the data room. Remove the sense that the business is held together by your personal force of will.

That doesn’t make valuation simple. It makes it more credible. And credible businesses tend to negotiate from a stronger position.

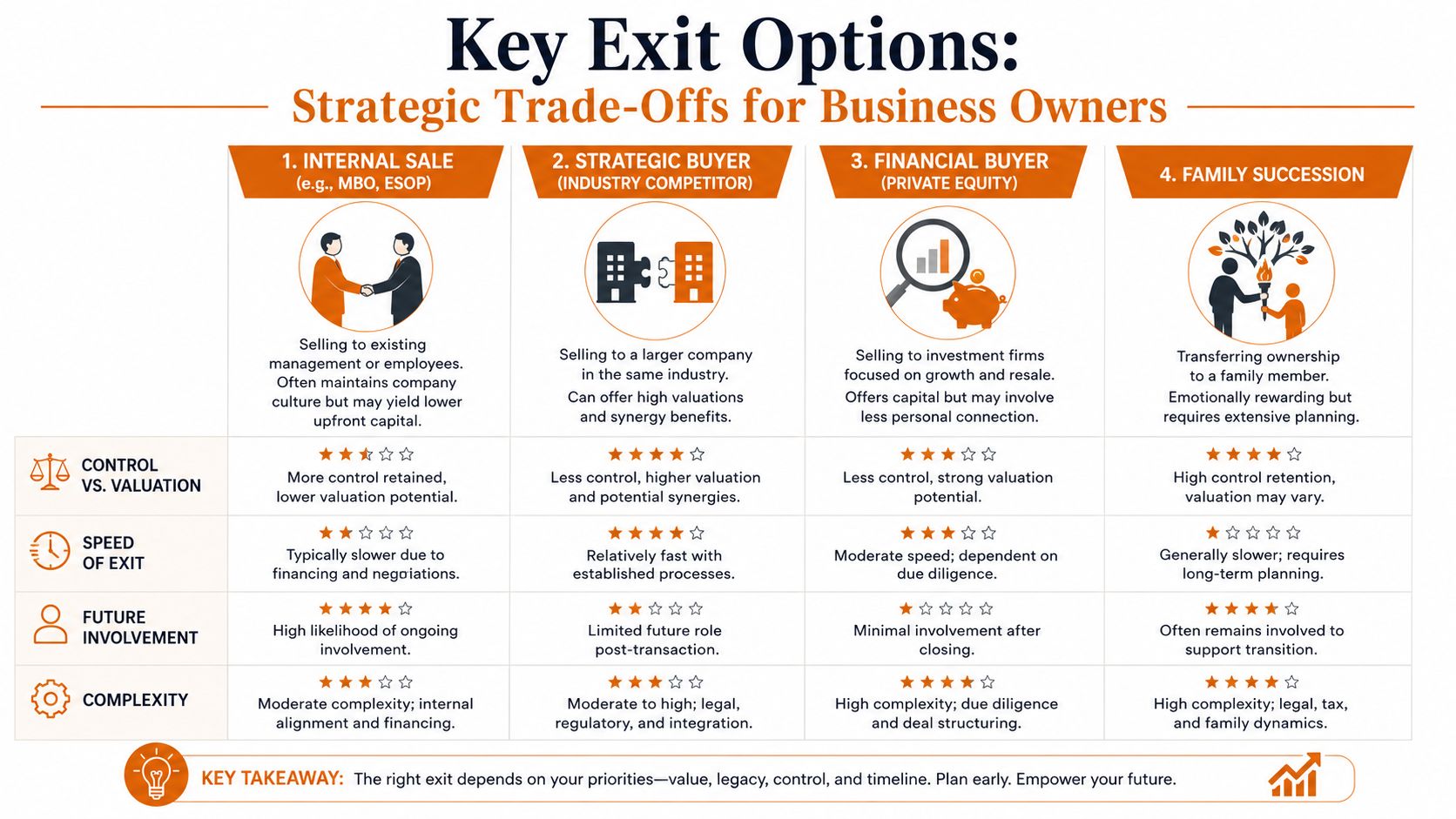

The right exit path depends on what you want to optimize. Price is one variable. It isn’t the only one.

Some owners care most about a clean break. Others care about preserving the team, keeping the business independent, or making sure the next owner doesn’t gut the culture. You can’t maximize every outcome at once, so the work is deciding which trade-offs you can live with.

A strategic buyer usually wants synergies. They may value your customer base, geography, product line, workforce, or route density more than a purely financial buyer would. That can support a strong headline number. It can also mean your legacy gets absorbed into a larger platform.

A private equity buyer looks at growth, cash generation, and the ability to scale. Some deals keep the owner involved for a period and can offer a second future payday if the platform grows and sells again. The trade-off is that private equity is disciplined and financially focused. Culture fit matters, but economics drive the deal.

A family succession can preserve identity and continuity in a way no outside sale can. It can also create emotional pressure that outside deals don’t. Questions of fairness, authority, readiness, and sibling dynamics have to be handled directly. Family transitions go badly when owners treat them as informal understandings rather than formal transactions.

An internal sale, whether to management or employees, often protects culture and rewards the people who helped build the company. It can be satisfying. It can also involve a slower path, more financing complexity, and a different mix of cash at closing versus future payments. If you’re weighing that route, this article on selling a business to employees lays out the practical considerations.

| Exit path | Best fit for | Likely tension |

|---|---|---|

| Strategic buyer | Owners seeking strong price and a defined exit | Legacy and integration control |

| Private equity | Owners open to a phased transition and growth story | Financial discipline and ongoing performance expectations |

| Family succession | Owners who value continuity and family legacy | Emotional complexity and governance |

| Internal sale | Owners who want cultural continuity for the team | Funding and timing challenges |

A few candid questions help sort this out quickly:

No path is universally the best. The best one is the one that fits your life after the transaction, not just your banker’s spreadsheet.

Owners sometimes wait too long to build an exit team because they don’t want a parade of advisors billing hours before there’s a deal. That instinct is understandable. It’s also expensive.

A good team doesn’t create complexity. It prevents the wrong kind. Each advisor sees a different category of risk, and those risks don’t stay neatly separated. Tax affects structure. Structure affects negotiations. Negotiations affect your personal planning. Personal planning affects whether an offer is enough.

Start with a valuation professional who can help establish a defendable baseline and identify the factors pushing value up or down. The goal isn’t just a number. The goal is understanding what a buyer is likely to challenge.

A transaction-focused tax advisor is different from the person who handles routine tax filings. Deal structure, entity setup, proceeds planning, and timing can all affect what you keep after closing.

An M&A attorney handles more than documents. Good deal counsel spots risk allocation issues, closing conditions, representations, indemnities, and the places where “standard language” becomes very non-standard once money is at stake.

A wealth manager or financial planner helps answer the question owners often avoid until late in the process: “What does this sale need to do for my life?” That includes income planning, liquidity, risk, and family priorities after the business changes hands.

For owners trying to understand where an advisor fits before hiring one, this explainer on what an exit planning advisor does is a sensible starting point.

You’re still the decision-maker. The point of the team is not to take control away from you. It’s to keep you from making a once-in-a-lifetime decision with half the information.

The best time to involve specialists is before urgency shows up.

Owners who try to quarterback all of this alone often end up negotiating with incomplete facts. They may still close a deal. They just don’t close the best version of it.

Most exits that work well weren’t assembled in a hurry. The owner had time to improve the business, fix what buyers would flag, and get clear on what outcome they wanted.

This visual gives the broad sequence.

At three-to-five years out, the work is strategic. Clean up reporting. Identify weak spots in the management bench. Document how work gets done. Start treating the business as an asset that must be transferable, not just profitable.

At one-to-two years out, the focus gets sharper. Owner dependency, contract quality, customer mix, and diligence readiness start to matter in a concrete way. A major benchmark is customer concentration. If any single customer accounts for more than 15% of total revenue, valuation can suffer and buyer diligence gets more difficult, according to Sofer Advisors’ discussion of exit readiness and concentration risk. The practical fix isn’t overnight. Owners generally need a 12 to 18 month effort to diversify exposures and build clearer revenue reporting for buyers in that same source.

That’s also the phase where you should start pressure-testing your story. Can someone else explain the business clearly? Are contracts current? Are margins understandable? Can your team answer operating questions without looking at you?

A useful outside perspective on timing and preparation is this short video.

In the final stretch before market, owners need discipline. Keep performance steady. Don’t get so consumed by the process that the business slips. Late surprises in financials, customer issues, or team stability can swiftly affect their position.

Use this as a working list, not a one-time exercise.

Buyers can tolerate issues they understand. They discount issues they discover late.

The timeline matters less than momentum. If you start early, you have choices. If you wait until you’re tired, sick, distracted, or suddenly approached by a buyer, choices narrow quickly.

Owners rarely sabotage an exit through one dramatic mistake. More often, they let small problems pile up until the business looks riskier than it really is.

One common trap is waiting for perfect timing. Owners tell themselves they’ll do one more year, land one more big account, or push through one more busy season. Sometimes that works. Sometimes life, health, or market conditions make the decision for them. A better approach is to prepare while you still have energy and advantage.

Another is letting the business sag during the process. Once talks begin, owners can get distracted by meetings, requests, and documents. Customers still need service. Managers still need direction. If performance slips, buyers notice quickly.

The third is confusing emotional value with market value. Pride is earned. It just isn’t a pricing method. Owners who hold both truths at once tend to negotiate better because they can stay firm without becoming unrealistic.

A few practical habits help:

An exit should feel intentional. Not rushed, not forced, and not defined only by the purchase price.

If you’re starting to think seriously about your next chapter, The Owner’s Shortlist is a practical place to begin. It offers plain-English guides and a curated directory of vetted specialists across valuation, tax, legal, succession, financing, and related decisions, so you can understand your options before engaging the right expert.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

Practical guide to wealth planning for high net worth individuals with business-tied wealth. Master 2026 tax, estate, and liquidity strategies for lasting

July 18, 2026

Discover how to make selling business to employees a success in 2026. Our guide covers ESOPs, direct sales, valuation, tax, financing, and a step-by-step

July 12, 2026

Discover what is financial due diligence & its critical role when selling your business. Our 2026 guide covers the process, red flags, and prep tips for owners.

July 7, 2026

Planning to sell to your best employees? Here's why it often fails, and how an ESOP solves the financing problem while giving all your crew a stake.

July 5, 2026