What Is Financial Due Diligence: Your 2026 Guide

Discover what is financial due diligence & its critical role when selling your business. Our 2026 guide covers the process, red flags, and prep tips for owners.

July 7, 2026

July 12, 2026

You may be in that uneasy middle ground right now. The business is healthy, customers still call because they trust your name, and a few employees have been with you long enough to remember when the office had folding chairs and one printer that jammed every day. You’re not just asking, “What can I get for the company?” You’re also asking, “What happens to the people who built it with me?”

That’s where selling business to employees becomes more than a technical exit route. For a lot of owners, it’s the first option that feels financially serious without feeling emotionally careless. The catch is that most articles jump straight to ESOPs and skip the hard part for smaller owner-operated companies. Your team may be capable of taking over. They just may not have the cash.

Owners rarely bring this up first as a pure finance question. It usually starts with a person. The service manager who steadied the business during a rough year. The office lead who knows every customer by voice. The crew chief who protects your reputation when you’re not on site.

Selling to employees can protect the part of the business that doesn’t show up neatly on a balance sheet. It can keep decision-making close to the people who understand the work, preserve relationships with customers and vendors, and reduce the odds that an outside buyer strips out what made the company work in the first place. If you’ve wondered what happens to employees when you sell a business, that’s often the heart of this conversation.

This path isn’t just sentimental. Employee-owned companies are more than 21% more likely to remain in business during economic downturns, with fewer closures, fewer layoffs, and higher retention, according to Harvard Business School’s review of employee-owned companies in downturns.

That matters because a good exit isn’t just the day you sign. It’s whether the company still stands after you leave.

Practical rule: If your biggest fear is watching a buyer break the culture, cut the team, or move the business away from its roots, an internal sale deserves a real look before you default to a third-party process.

Not every loyal team becomes a strong ownership group. Some employees are excellent operators but don’t want the pressure of debt, governance, or hard decisions. Others want ownership in theory but not in meetings, reporting, and accountability.

That’s why the best internal sales start with two honest questions:

When owners are clear on those answers, the rest of the planning gets simpler.

The menu is broader than most owners think. Some options fit a larger company with strong cash flow and formal leadership. Others fit a smaller business where a few key people can run operations but can’t write a large check.

Near the top end of the market, ESOPs are no niche idea. The U.S. ESOP market reached 6,525 plans by 2023, covering more than 15 million participants and holding about $2.0 trillion in assets, according to the Department of Labor employee ownership report to Congress. If you want a plain-English primer first, this overview of what an ESOP exit is is a useful starting point.

Here’s the visual version before we get practical.

1. Employee Stock Ownership Plan

An ESOP is a qualified retirement plan that buys company stock for employees. In practice, it’s often best for companies with enough scale, reliable cash flow, and a willingness to handle a more formal structure with trustees, legal documents, valuation work, and ongoing administration.

Best fit: companies with enough size and administrative tolerance to justify the setup.

Main trade-off: tax advantages can be strong, but complexity is real.

2. Management buyout

A management buyout usually means a small group of current leaders buys a controlling stake. This often works when your leadership bench is stronger than your broader employee base, and you already know who can run the company day to day.

Best fit: a business with proven managers who already act like owners.

Main trade-off: concentrated leadership can make decisions faster, but it may exclude the wider employee group.

Before comparing the rest, it helps to hear one outside perspective.

3. Direct sale to key employees

This is the plainest version. You sell shares or membership interests directly to one or more employees. It can be clean and flexible, especially when you have one standout successor or a small ownership group in mind.

Best fit: smaller firms where trust is high and the buyer group is obvious.

Main trade-off: simple on paper doesn’t mean easy to fund.

4. Seller-financed internal sale

In this structure, you act as the bank for part or all of the deal. The employees buy over time, and you get paid through a note from future business performance rather than a large lump sum on day one.

Best fit: smaller owner-operated companies where the team can run the business but can’t raise enough cash upfront.

Main trade-off: this can solve the affordability problem, but it keeps you financially tied to the business for a period after closing.

5. Gradual equity transfer

This path spreads ownership over time. Employees earn or buy in through staged transfers, bonus redirection, or phased purchases tied to milestones. It often works well when the owner doesn’t want to leave all at once.

Best fit: owners who want a measured handoff of leadership, ownership, and control.

Main trade-off: patience helps, but slow transfers can create confusion if the rules aren’t written clearly.

| Option | Best For | Complexity | Owner Tax Benefit |

|---|---|---|---|

| ESOP | Larger companies with stable cash flow and appetite for formal administration | High | Potentially strong, especially if structured to qualify for ESOP-related tax treatment |

| Management buyout | Businesses with a proven leadership team | Moderate | Depends on entity type and sale structure |

| Direct sale to key employees | Small firms with obvious internal successors | Low to moderate | Depends on structure, usually less specialized than ESOP planning |

| Seller-financed sale | Companies where buyers lack cash but future cash flow is solid | Moderate | Depends on note structure and broader tax planning |

| Gradual equity transfer | Owners who want a phased transition | Moderate | Depends on timing, entity type, and transfer design |

A lot of owners think the only serious employee sale is an ESOP. That’s not true. For many smaller companies, a narrower internal deal is more realistic and less cumbersome.

The question I hear most is blunt and fair: “If I sell internally, am I taking less?” Not necessarily.

The standard isn’t “friendly price.” The standard is fair market value, then building a deal your buyers can carry. For employee buyouts, businesses under $1-2M in revenue are typically valued using Seller’s Discretionary Earnings, while businesses over $2M typically use EBITDA, based on OffDeal’s guide to selling a business to an employee. That same source notes that selling to employees doesn’t require accepting a lower price, because the deal can be funded through the company’s future cash flow.

Think of SDE as a way to measure the business with the owner still in the picture. It starts with earnings, then adjusts for the owner’s compensation and certain non-recurring or personal expenses. That makes sense when the owner still wears many hats.

A plumbing company, small manufacturer, or local service firm often fits here. If the business depends heavily on your day-to-day involvement, SDE usually tells the more honest story.

A few practical implications follow:

EBITDA works better when the company functions more like a managed enterprise than an owner-centered job. It strips out financing and certain accounting items to focus on operating performance.

The easiest analogy is this: SDE values the whole truck, including the driver who also owns it. EBITDA looks more at the engine of the business once a management team is already in place.

Don’t fight over the formula before you’ve cleaned the books. Messy financials cause more valuation arguments than the choice between SDE and EBITDA.

For an internal sale, the most useful valuation isn’t just defensible. It’s financeable. A number can be technically fair and still fail if debt service would choke the company after closing.

Casual planning usually breaks down. Owners often focus on price first, then discover that structure changes net proceeds and control more than they expected.

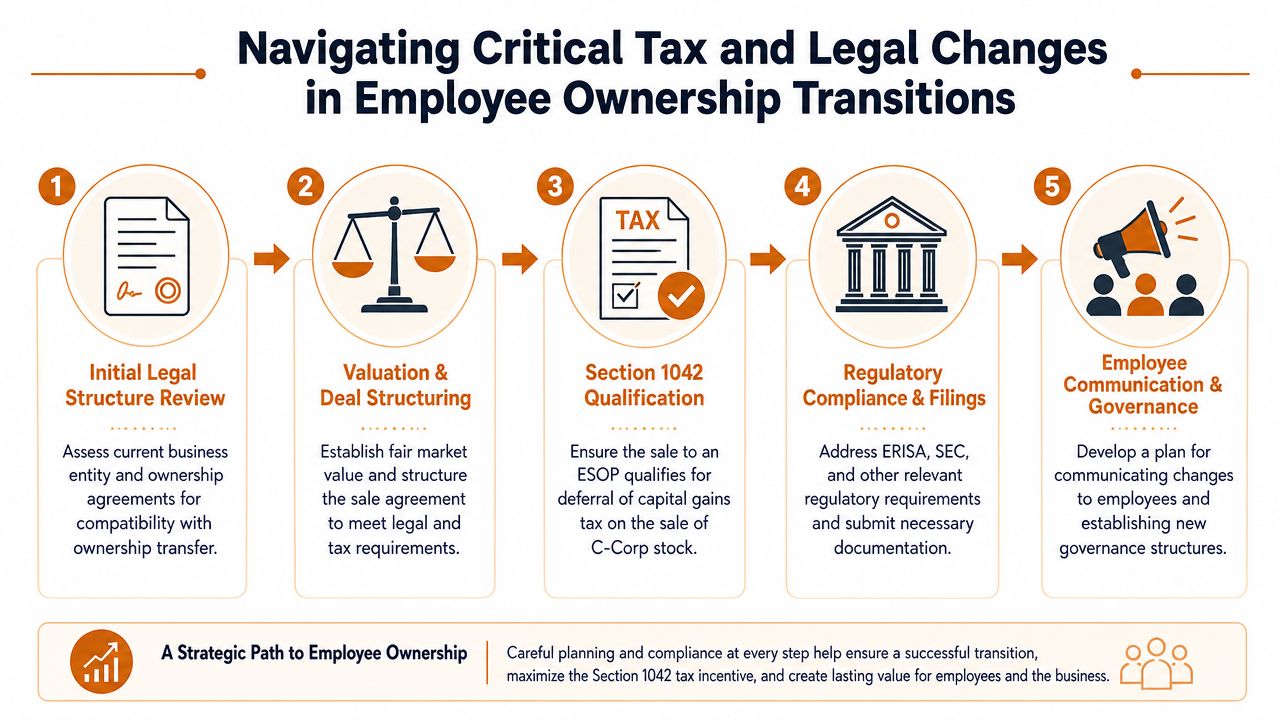

For C-corporation owners, one of the strongest tax incentives in this area is the Section 1042 rollover. Selling to an ESOP can allow an owner to defer 100% of capital gains taxes if the company allocates at least 50% of voting stock and 50% of the value of non-voting stock to the ESOP, according to Project Equity’s explanation of employee ownership versus selling to an outside buyer.

That matters because the seller can reinvest the full pre-tax proceeds into qualified replacement property rather than losing part of the sale value to immediate capital gains tax. In plain English, it can preserve more of the sale proceeds for your next chapter.

That doesn’t mean every owner should force an ESOP. It means the tax conversation belongs on the table early, before you lock yourself into the wrong path.

The legal change that owners feel most isn’t a clause. It’s governance.

If you’ve run the business by instinct, speed, and direct authority, employee ownership usually moves you toward a more structured model. Decisions get documented. Roles get defined. Ownership rights and management authority need to be separated with care.

Here are the friction points that matter most:

The legal documents shouldn’t just close the deal. They should prevent the next argument.

A strong structure gives you two things at once. It protects the seller from ambiguity and protects the employee buyers from misunderstandings about what they’re getting.

This is the section most owners need most. Not because the ideas are exotic, but because in it good intentions collide with arithmetic.

Your employees may be the right successors and still have no realistic way to buy you out with after-tax cash. That’s the affordability gap, and it’s one of the biggest reasons internal sales stall. As noted in Synergy Business Brokers’ discussion of selling your business to an employee, employees rarely have the cash for a direct purchase, which is why structures like seller financing and buy-ins funded through forgone bonuses come up so often. If you want the mechanics in plain English, this explanation of how seller financing works is useful background.

The awkward version goes like this. The owner names a fair price. The employee says they’re honored. Then everyone avoids the obvious question: “With what money?”

That silence kills deals.

Many internal buyers are rich in competence and poor in liquidity. They may have home mortgages, kids in school, and little appetite for personal guarantees. That doesn’t make them weak buyers. It means the structure has to fit the reality of a working person, not a private equity fund.

Seller note

This is the workhorse solution. You sell the business and take back a promissory note. The company’s future earnings fund payments over time.

Why it works: it bridges the cash gap without forcing employees to raise a large amount upfront.

What to watch: the note terms have to leave enough oxygen in the business. If payments are too aggressive, everyone suffers.

Bonus-funded buy-in

Some owners let employees direct forgone bonuses over a period of years into equity purchases. Instead of writing a large check once, the buyer group builds ownership gradually.

Why it works: it matches the pace of wealth-building available to employees.

What to watch: expectations have to be documented carefully, especially around valuation resets and what happens if a participant leaves midway.

Hybrid structures

A lot of practical deals combine methods. For example, a key manager might put in some personal cash, the owner carries a note, and the rest of the transfer happens in stages. This can reduce strain on both sides.

Here are the design questions that matter more than cleverness:

If your employees can only buy the company in a spreadsheet and not in real operating conditions, the structure isn’t done yet.

For smaller companies, this is often the most sensible path in selling business to employees. Not glamorous. Just workable.

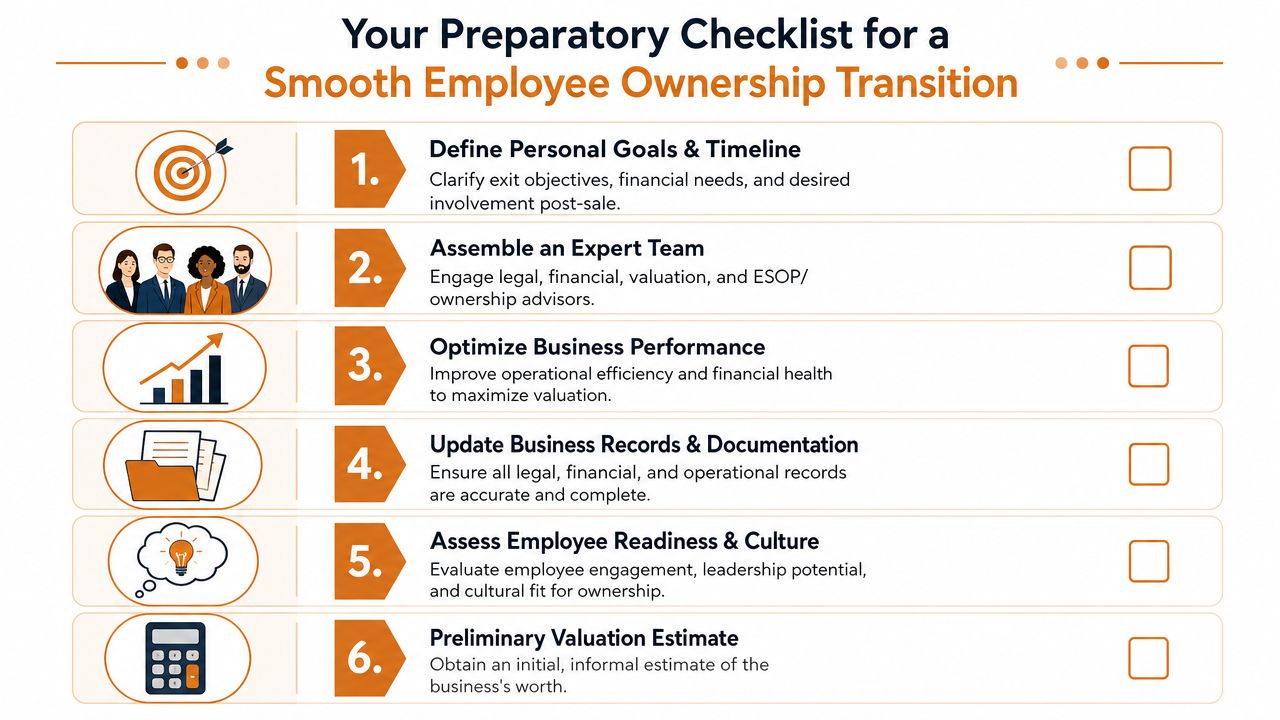

A smooth internal sale starts before anyone signs a letter of intent. Owners who prepare early usually have more options, cleaner negotiations, and fewer unpleasant surprises.

A good checklist doesn’t make the deal happen. It makes the key issues visible while there’s still time to fix them.

Selling to employees can be a strong succession path if your goals include continuity, legacy, and rewarding the people who helped build the company. It can also become messy fast if you skip the mechanics. The biggest trap is assuming a willing team automatically equals a financeable deal.

Call in a valuation specialist when you need a defensible number tied to real cash flow. Bring in a tax advisor before you choose the sale structure, because net proceeds can change materially depending on the path. Involve an attorney once you start discussing ownership rights, governance, notes, or buy-sell terms. Talk with a financing advisor or lender when the affordability gap becomes the central problem. If you’re leaning toward an ESOP, add an ESOP-specific advisor early rather than trying to retrofit the process later.

The best internal sales aren’t improvised. They’re designed.

If you’re weighing selling business to employees and want help finding the right valuation, tax, legal, financing, or succession specialist, The Owner’s Shortlist gives long-time owners a practical place to start. It’s a curated directory and editorial resource built for owner-operated businesses, with plain-English guides and direct access to vetted specialists without lead forms or middlemen.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

Discover what is financial due diligence & its critical role when selling your business. Our 2026 guide covers the process, red flags, and prep tips for owners.

July 7, 2026

Planning to sell to your best employees? Here's why it often fails, and how an ESOP solves the financing problem while giving all your crew a stake.

July 5, 2026

An ESOP lets you sell your business to your employees and defer most of the tax. Here's how it works, who qualifies, and when it makes sense.

July 5, 2026

Plumbing maintenance agreements are the revenue type buyers pay the most for. Here's how to build them and what they do to your sale price when you exit.

July 4, 2026