Succession decisions that protect value, family, and optionality

Succession is not one decision. It's a set of choices about ownership, leadership, family fairness, and cash out. Here's how to compare your paths.

June 16, 2026

July 13, 2026

You may be in a familiar spot right now. The business is healthy, the family depends on it, and you know your personal estate plan can’t sit in a separate folder from your succession decisions anymore. If ownership, control, tax exposure, and family expectations aren’t coordinated, the documents may look finished while the actual risk remains unresolved.

That’s why choosing an estate planning law firm isn’t just a legal hire. For an owner-operated company, it’s a business continuity decision. The right firm helps protect leadership transition, preserve value, and reduce the odds that your family or key employees end up sorting through avoidable conflict under pressure.

A lot of owners assume any competent lawyer can handle estate planning. That assumption works for simple documents. It fails when the estate includes a closely held business, family members with unequal roles, key employees, real estate, partner obligations, and a future transfer that has to work both legally and operationally.

If you own a company, your estate plan isn’t just about who gets what. It has to answer harder questions. Who controls the business if you’re incapacitated? Who owns it if your children don’t all work in it? How does a buy-sell agreement interact with your trust, operating agreement, or shareholder documents? What happens to voting control while the estate is being administered?

A general practitioner may draft a will that distributes your ownership interest. A specialist looks deeper. They ask whether the transfer structure preserves the company as a going concern, whether management authority is clear, and whether the plan creates friction between active and non-active heirs.

That distinction matters in family firms where “fair” and “equal” aren’t the same thing. An owner who leaves the business equally to all children may think they’ve treated everyone fairly, while inadvertently creating a governance problem for the child who runs the company.

Practical rule: If the business is the largest asset in your estate, your lawyer should treat the succession plan as a core legal project, not a side note to your will.

Owners who are weighing continuity decisions often benefit from thinking through the broader trade-offs first. A useful framing appears in this guide on succession decisions that protect value, family, and optionality.

Specialization should be measurable, not self-declared. Expert guidance suggests estate planning should represent at least 75% of an attorney’s active caseload, and a generalist handling 5 estate plans a year lacks the nuanced knowledge of state-specific rules and business asset protection strategies that a dedicated specialist possesses, as noted in this guidance on finding an estate planning attorney in California.

That threshold is useful because business succession is full of moving parts. The attorney needs to understand how entity documents, beneficiary designations, trusts, powers of attorney, leadership authority, and tax-sensitive transfers fit together. If estate planning is only a small slice of their practice, they may know the forms without mastering the interactions.

A strong estate planning law firm for business owners also knows when not to oversimplify. Sometimes a straightforward plan is the right answer. Sometimes a “simple will package” creates downstream confusion because it ignores the company’s governance, key person risk, or the family’s actual intentions. The point isn’t complexity for its own sake. The point is fit.

Owners often ask for “someone experienced.” That sounds sensible, but it’s too vague to help you choose. The better question is whether the firm has the right kind of experience for a business-owning household.

The market is large and mature. The United States had 203,660 estate lawyers and attorneys businesses as of 2025, with 0.6% growth from 2024 and an average annual growth rate of 0.5% from 2020 to 2025, according to IBISWorld’s estate lawyers and attorneys industry data. In a market that established, specialization can be identified and verified. The same source notes that top-tier groups are often recognized by resources such as Chambers High Net Worth, and some firms have been recognized for nearly 20 consecutive years.

That means you don’t need to settle for vague claims. You can ask for concrete signs that the firm works in this area consistently and at a high level.

Here’s what deserves a closer look:

A polished website doesn’t tell you much on its own. Bios matter more. Read for the kind of work described, not just years in practice. Does the attorney talk about business succession, trust administration, ownership transfers, and coordination with other advisors? Or is estate planning listed beside unrelated areas with equal emphasis?

A mature firm should also be able to explain its process in plain English. If you ask how they handle a business-owning client and the answer is mostly jargon, that’s not sophistication. It’s often a sign that the work is template-driven or poorly scoped.

A quick comparison helps:

| What to look for | What to be cautious about |

|---|---|

| Specific discussion of business interests and transition issues | Generic “asset protection” language with no detail |

| Clear explanation of who on the team handles what | Everything sounds partner-led until documents arrive |

| Willingness to coordinate with your other advisors | A firm that wants to work in isolation |

| A defined review and update approach | A one-time drafting mindset |

If a future sale is one possible path, it also helps to understand the legal work that tends to surface in ownership transitions. This overview on whether you need an attorney to sell a business is a useful companion because many estate planning choices intersect with sale readiness.

Good firms don’t just produce documents. They reduce ambiguity about control, authority, and what happens next when life changes.

The fastest way to waste time is to start with a broad web search and treat every estate planning law firm as interchangeable. Owners usually get better results when they begin with professionals who already understand the business and the household balance sheet.

One of the most reliable channels is referral through your existing advisory team. A common operational method for successful law firms is establishing strong referral relationships with accountants and financial advisors, which creates a pipeline of clients whose needs are already understood, as described in this discussion of succession planning methods for determining the value of a law practice.

That makes practical sense. Your CPA often knows where the complexity sits. Your financial planner may know whether family wealth is concentrated in the business, real estate, or retirement accounts. Those advisors also tend to notice which attorneys communicate well and which ones create cleanup work.

Start your shortlist this way:

If you want a more structured way to compare specialists, review how The Owner’s Shortlist works.

Once you have a few names, don’t book consultations blindly. Review each firm with a business-owner lens.

Focus on these signals:

A shortlist should be short. Three or four candidates is enough. More than that usually creates noise, not clarity.

Your aim isn’t to find the lawyer with the broadest marketing footprint. It’s to find the firm that can think clearly about ownership, control, family dynamics, and implementation.

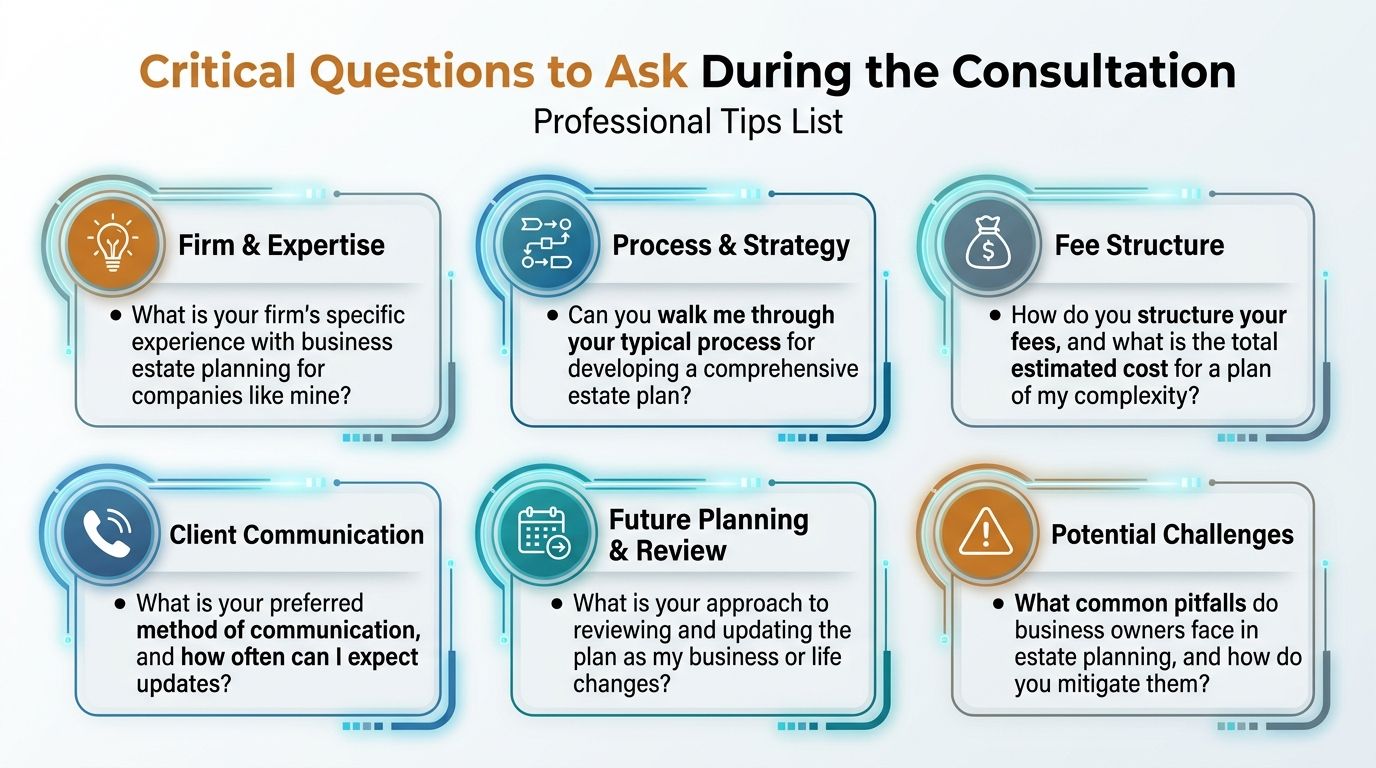

The consultation tells you more from process than polish. Owners often leave impressed by credentials and still miss the question that determines whether the plan will work in real life.

A short overview can help you frame the conversation before you go in:

A productive consultation feels less like a sales pitch and more like a working session. The attorney should ask about your family, your ownership structure, the people who run the business, and what would happen if you were absent for an extended period.

Use questions like these:

Listen for specificity. A strong answer will acknowledge trade-offs. For example, leaving ownership equally may feel fair but create governance tension. Naming one child as operator may preserve continuity but require balancing steps elsewhere in the estate plan.

This is the question I’d insist on asking in every consultation:

Will you handle the deed transfers and asset reassignments, or is that my job?

That question matters because drafting a trust and funding a trust are not the same thing. Up to 70% of revocable living trusts fail because assets are never formally transferred into them, according to this discussion of questions to ask before choosing an estate planning attorney.

For business owners, trust funding can include much more than a home deed. It may involve ownership interests, assignments, related schedules, and coordination with financial institutions or internal company records. If the firm treats funding as your problem after signing day, you need to understand that before you hire them.

Not every good firm handles every implementation task in-house. That’s fine. What matters is clarity.

A strong answer usually includes some version of the following:

| Question area | Strong answer | Weak answer |

|---|---|---|

| Business succession | Explains how they align estate documents with governance and family roles | Says they’ll “put everything in the trust” |

| Fees | Gives a clear scope and explains what may fall outside it | Stays vague until after engagement |

| Communication | Identifies your main contact and review points | “Call us if you need anything” |

| Funding and transfers | States exactly what they handle and what you must do | Assumes you’ll figure it out later |

A consult should leave you with fewer gray areas, not more.

If the attorney can explain difficult trade-offs without slipping into canned language, that’s a strong sign. If every answer sounds universally reassuring, keep pushing. Estate planning for owners involves choices. Good counsel doesn’t hide that.

Some firms disqualify themselves quickly if you know what to watch for. The biggest mistakes usually show up early, long before the documents are signed.

Be cautious if the attorney doesn’t spend much time asking about the business itself. If they move straight into wills, trusts, and powers of attorney without digging into ownership structure, management roles, family involvement, or successor readiness, they may be treating your company like just another line item on a balance sheet.

Another warning sign is a one-size-fits-all recommendation. Owners differ. Some want to transfer to children. Some want managerial continuity first and ownership transition later. Some need flexibility because a sale remains possible. A firm that reaches for the same package every time may be selling efficiency, not judgment.

Watch for communication habits too:

Outdated documents are a primary pitfall of ineffective estate planning. Successful firms actively monitor and promote updates to reflect life changes, which is highlighted in this article on estate planning law firm efficiency and client retention using data.

That issue matters because owner circumstances change constantly. Businesses add partners, refinance property, revise agreements, hire successors, and shift compensation structures. Families change too. Marriages, divorces, births, deaths, and health events can alter the plan’s effectiveness.

A firm that treats estate planning as a one-time transaction may leave you with technically signed documents that no longer match reality. The red flag isn’t just silence after delivery. It’s the absence of any review discipline at all.

If a firm can’t describe how they help clients keep documents current, they’re not offering stewardship. They’re offering paperwork.

Once you’ve chosen a firm, the work becomes more concrete. This stage should feel orderly. If it feels murky, pause and get clarity before moving money or signing broad authority documents.

Read the engagement letter carefully. You’re looking for scope, exclusions, timeline expectations, and who is responsible for implementation steps. If business interests are involved, make sure the engagement reflects that. “Estate plan” can mean very different things depending on whether the work includes reviewing entity documents, coordinating with tax advisors, or assisting with transfers.

This is also the moment to confirm how the relationship will function after signing. Will the firm notify you when reviews are advisable? Is there a maintenance process? Who should your family or management team contact in an emergency?

A good attorney can move faster and think more clearly when you provide complete information early. Gather the documents that shape both ownership and family outcomes:

There’s a broad planning gap in the market. While 56% of Americans believe estate planning is important, 73% of respondents in a detailed survey do not have a documented estate plan, according to these estate planning statistics from LegalZoom. For a business owner, closing that gap isn’t just personal housekeeping. It helps prevent legal gridlock and family conflict around the asset that often matters most.

The right estate planning law firm won’t just produce documents. It will help translate your intentions into a structure your family, your company, and your advisors can use.

If you’re sorting through succession, legal structure, tax exposure, or how to find the right specialist without wasting weeks on generic searches, The Owner’s Shortlist is a practical place to start. It’s built for long-tenured business owners who need vetted specialists and plain-English guidance before they engage an attorney, advisor, or tax professional.

Tell us your situation. We'll connect you with a specialist who works with owners like you. One conversation, no sales pressure.

Succession is not one decision. It's a set of choices about ownership, leadership, family fairness, and cash out. Here's how to compare your paths.

June 16, 2026

Passing a business to your kids is more complicated than leaving it to them in a will. Here's what the process looks like and where it usually goes wrong.

April 3, 2026